Weekend Update #185

Thank you for your continued support and engagement. Each week, we're sharing what companies we're researching and the what, the who and the how that we think makes the companies interesting and unique. This roundup is brought to you weekly by a group of interns, creative minds, artists and investors who believe that through best in class investing along with the democratization of financial education we can do great things together. Enjoy, Explore and Share.

Major indexes ended the second quarter on a high note, with the S&P 500 and Nasdaq finishing the first half of the year up an impressive 15% and 20%, respectively. Despite a relatively quiet news flow leading up to the Fourth of July holiday, market narratives were shaped by key macroeconomic releases along with earnings reports from S&P 500 heavyweights.

On Wednesday, the Commerce Department reported a significant decline in new home sales, plummeting to a six-month low and marking the largest drop in over 18 months. The 16.5% year-over-year slump in May, combined with a 16-year high in supply, signaled the housing market’s sensitivity to interest rates and fueled calls for the Federal Reserve to begin cutting interest rates.

To further support the case for interest rate cuts, the Federal Reserve’s preferred inflation gauge, the Core PCE price index, fell to its lowest level in 2024 on Friday, reinforcing June’s strong inflation data. Although the 0.1% month-over-month and 2.6% year-over-year increases were in line with expectations, the Federal Reserve will need to see further readings of this sort before it gains confidence that inflation is sustainably on a path to 2%. Interest rate traders on the CME are pricing in the first cut in September.

In company-specific news, shares of FedEx jumped as much as 15% on Wednesday after the delivery giant announced better-than-expected earnings guidance and considered divesting its freight trucking business. FedEx CEO Raj Subramaniam attributed the success to cost-cutting measures and unit consolidation. Meanwhile, Nike stock plunged as much as 20% after the retailer cut its full-year guidance, citing soft sales in China and an expected 10% sales drop in the current quarter.

Next week, June’s jobs data will take center stage with JOLTS data released on July 3 and Unemployment and Nonfarm Payrolls data on July 5, providing key insight into the other half of the Federal Reserve’s dual mandate.

Weekly Performance

S&P 500 5,459.92 +0.01%

Nasdaq 17,732.60 +0.52%

Dow Jones 39,122.94 -0.16%

Thank you Blue Room Analyst SPENCER WOOTTEN.

Although flat for the week, the S&P 500 closed near its all-time high. In fact, the market strength, which has been largely driven by the Artificial Intelligence wave, led to one of the best performing first-halves of an election year. While many Fund One long positions, both AI-related like Nvidia and non-IT companies like Eli Lilly and Sweetgreen, outperformed the index, overall performance has been hampered in large part by short positions that have also moved with the market (e.g. Arm and Cava). Despite this, there remains plenty to be hopeful about moving into the second half of the year.

The team looks forward to diving deeper into recent Fund performance and our outlook for the remainder of the year during our next quarterly investor call. Wishing you a Happy Independence Day!

Thank you Blue Room Investing President JOHN FENLEY

Executive Summary

The primary shortfall in the quarter was the poor outlook that Nike provided for F2025. In the first quarter, Nike expects sales to decline 10%. Last quarter, management indicated that 2H25 would be down low single digits HoH, but revised this outlook to be down 7%-9%. Last quarter, the company originally guided to marginal growth for F25. Now, Nike forecasts a sales decline in the mid-single-digits range, while both Blue Room and consensus expected sales to grow (BR: approx. +2.26%; Street: approx. +1.00%). Nike is looking to mitigate forward headwinds by accelerating its plan to restrict supply of “classic” footwear franchises around the world, while targeting 2H25 for new franchise releases to support sales.

CFO Matt Friend indicated that Nike’s internal estimate for next year was lowered by several headwinds incurred in this year’s fourth quarter. Those headwinds included declines in lifestyle category products through the online channel, worsening FX, and global demand uncertainty. Nike had digital channel weakness in classic footwear franchises, but also saw strength in these same franchises in the multi-brand retail channel. Nike Direct was down 7%, Nike stores were down 2%, Nike digital was down 10%, but Wholesale revenue grew 8%. This suggests a trend that we’re seeing broadly across retail, where the consumer is choosing to shop in-person rather than online. China brick and mortar traffic did decline double-digits year over year, which suggests that shopping frequency may be slowing.

The company, however, should have an opportunity to stabilize sales trends in sports performance categories with Nike showing “strong gains'' in performance products during 4Q24. In basketball, the Sabrina one has taken 2 points of share across the US basketball market. (Nike also described female’s fitness as one of the largest market opportunities for the company, targeting the market share of lululemon and other athleisure brands, as the company described leggings as a key focus that was up double-digits in Q4). The Pegasus 41 launch had better-than-expected sell-through in wholesale and direct channels. They also will support the running category with Pegasus Premium and Vomero 18 in the second half of next year, as the company looks to stabilize its running market share. Lastly, the Air Max Dn launched in the quarter to be a top ten lifestyle franchise in the men’s business. Another example of Nike’s strategy to manage key franchise supply working is the Pegasus portfolio transition with Vomera, Invincible, Infinity, and Structure growing double digits QOQ.

Greg Peterson — Head of Investor Relations

So, good evening to those of you joining us on the webcast. Welcome to AGCO's Fourth Annual Technology Event. My name is Greg Peterson. I head up Investor Relations for AGCO.

This year, we have two specific objectives for our technology event. The first is to demonstrate the significant progress we've made to some very aggressive technology deployment targets which culminate with being autonomous across the crop cycle by 2030. And the second objective is to highlight the significant benefit that AGCO is going to enjoy on both our top-line and our margins from growing our precision ag business.

So with those two important objectives in mind, let's take a look at what's ahead of us tonight. So, Eric Hansotia, our President, Chairman and Chief Executive Officer will start with a brief overview of our strategy and explain how growing our precision ag business fits in with that strategy. Seth Crawford, who runs our new PTx organization, he's going to give us an insight to that new organization, and then he'll also give us a heads-up on what's going to happen tomorrow at the field event.

Andrew Sunderman is here tonight. Andrew's the newly appointed General Manager of our PTx Trimble joint venture. Andrew's going to talk about the first 100 days of that joint venture, and he's going to give us an overview of the products and services that the joint venture's providing. So, they will give you kind of a heads-up in terms of the technology you're going to see demonstrated tonight.

And then, Damon Audia, our Chief Financial Officer, will finish up our prepared remarks, and then we'll finish off the program. Damon's going to cover the restructuring announcement that we published yesterday, so he'll spend a little bit of time giving us a little more color on that. And then, we'll finish the session with about 15 minutes of Q&A. And then following that, dinner.

So, let me go ahead and handle the Safe Harbor information. Tonight, we're going to refer to slides which are posted on our website, and as we go through the evening, we'll make forward-looking statements, including statements with respect to strategic plans, demand, product development, supply chain disruption, inflation, acquisitions, financial outlooks, input costs, sales, market share, margins, earnings, cash flow, and other financial metrics, as well as restructuring programs.

Actual results may differ materially from those suggested by these statements for a number of reasons, including declines in product demand and other adverse developments in agricultural and agricultural equipment industries, including those resulting from supply chain disruption, weather, exchange rate volatility, commodity prices, inflation, changes in product demand. And there are additional reasons under the risk factors in our Form 10-K for the year ended December 31st, 2023. We'll also disclaim any obligation to update any forward-looking statements except as required by law.

And finally, a replay of this meeting will be available on our website later this evening or tomorrow.

And with that, finally, Eric, please join us. Eric Hansotia, Chairman, President, and Chief Executive Officer.

Eric Hansotia — Chairman, President & Chief Executive Officer

Thank you. Well, welcome, everybody. Sure glad to have all of you here live. These next few days are going to be a lot of fun. We're going to do some learning together. We're going to get to see some product, talk about what it means for farmers and everything.

For those of you that are new, let's talk about why the focus on technology. Well, you see a really cool tractor out back here. It's a Fendt 1000. It's got 20 times the compute capacity of a Tesla car. So, that's what's already in there. And then some of the things that we're going to show you, a lot of what we're going to talk about, is really the heartbeat of the industry.

What do I mean by that? Well, I've been in this industry my whole career. In fact, my whole life, pretty much. And I spend a lot of time talking with farmers. And this is what they talk about. This is what they want to know about. How can you give me a technology solution that solves the squeeze I'm in? It helps me either increase my crop yields, I get more output, or it helps me better manage my inputs, my cost situation, or it helps me with sustainability, I'm getting more pressure on that. So, that's the main conversation farmers are focused on, is understanding a technology solution to the problems they face.

The Phillips Curve is Dead.

Long Live the Phillips Curve.

Economists constantly debate the validity of long-established and canonical models of the economy, and perhaps none has been the topic of more discussion than the Phillips Curve. Many economists have declared the Phillips Curve dead, with the relationship between unemployment and inflation that was seen prior to the Great Inflation of the 1970’s no longer observable in the United States. Others continue to hold onto the model as no suitable alternative has been able to better explain the connection between labor markets and inflation. But regardless of economists’ current stance on the issue, the Federal Reserve’s actions and financial markets’ perception of current economic conditions show that a traditional Phillips Curve framework of the economy is alive and well.

In 1958, A.W. Phillips noticed a relationship between wage inflation in the United Kingdom and the level of employment. Specifically, Phillips noted that when unemployment was high, wage inflation appeared low; when unemployment was low, wage inflation grew higher. This relationship is intuitive through the lens of supply and demand. If the unemployment rate is high, there is less marginal demand for labor, meaning companies don’t need to compete as much for workers, allowing them to slow the pace of wage increases. On the other hand, when the unemployment rate is low and there is strong demand for labor, companies must entice workers with greater wages in order to remain competitive.

Executive Summary

McCormick (MKC) shares rose markedly after the Company reported its second quarter earnings results, which outperformed analysts’ quarterly expectations for both earnings and sales. Despite the quarterly beat, McCormick reaffirmed its 2024 fiscal outlook with respect to sales growth, adjusting operating margin and adjusted earnings per share. Management’s commentary during the earnings call touched on several key themes, including investment and innovation, consumer trends, macroeconomic environment, product performance and market strategy, and future guidance. The overall sentiment was positive as the Company continues to make reliable progress towards its fiscal and long-term goals.

Executive Summary

Micron beat consensus expectations on revenue at $6.811 billion versus $6.668 billion expected. On a non-GAAP basis, Micron also beat earnings per share expectations at 62c versus 60c expected, however, on a GAAP basis Micron missed earnings by 7c, coming in at 30c versus 37c consensus expected. Primary drivers of the delta included higher COGS and higher operating expenses relative to street estimates.

Micron’s guidance beat topline expectations for the fourth quarter, coming in at $7.6 billion at the midpoint, versus $7.585 billion consensus and $7.671 billion Blue Room expected. GAAP operating expenses of $1.19 billion were slightly higher than the street’s $1.09 billion expected and taxes are implied to be over $600 million, whereas the street had $394. These factors drove a GAAP EPS miss at 61c versus 96c street expected (Blue Room had estimated $1.15). Non-GAAP EPS guidance was for $1.08 at the midpoint versus $1.07 street expected.

Price increases and product mix are driving profit leverage as the industry continues to see demand above supply, with AI-end markets primarily driving bit demand higher. Specifically, data center, PC, and smartphone end markets are highlighted as sources of end demand for continued pricing strength in the near-term. The company is still forecasting record revenue for fiscal 2025, with increasing profitability from mix. In the longer-term, Micron sees AGI (artificial general intelligence) driving a large demand for DRAM and NAND for all end markets.

Overall data center customer inventories have normalized, which is driving a low-single digit recovery in traditional server demand.

HBM is sold out for calendar 2024 and 2025 with pricing already contracted for the “overwhelming majority” of 2025 supply, which is positive QoQ newsflow, as last quarter only allocations were determined for 2025. This supports Micron’s confidence in record F2025 sales as DRAM represented about 70% of total revenue on average over the last four quarters. It also supports continued strength for the data center GPU end-market, which benefits Nvidia’s market position in that market.

PCs and smartphone customers have built up additional inventories to get ahead of further price increases, growth in AI PCs and smartphones, and rising demand for data center memory which will consume a large portion of manufacturing capacity. Additionally, AI PCs have 40% to 80% more DRAM content relative to today’s average PC. Microsoft’s minimum system requirement for Copilot+ PCs is 16GB DRAM

CEO, Mehrotra indicated his expectation for “several hundred million dollars” of revenue for HBM specifically, and for “several hundred billion dollars” in HBM revenue for F2025.

Negatives:

Despite certain AI-related end markets driving higher pricing and bit demand, the primary question around durability remains. Micron and memory in general tends to be highly cyclical and sensitive to changes in the demand outlook.

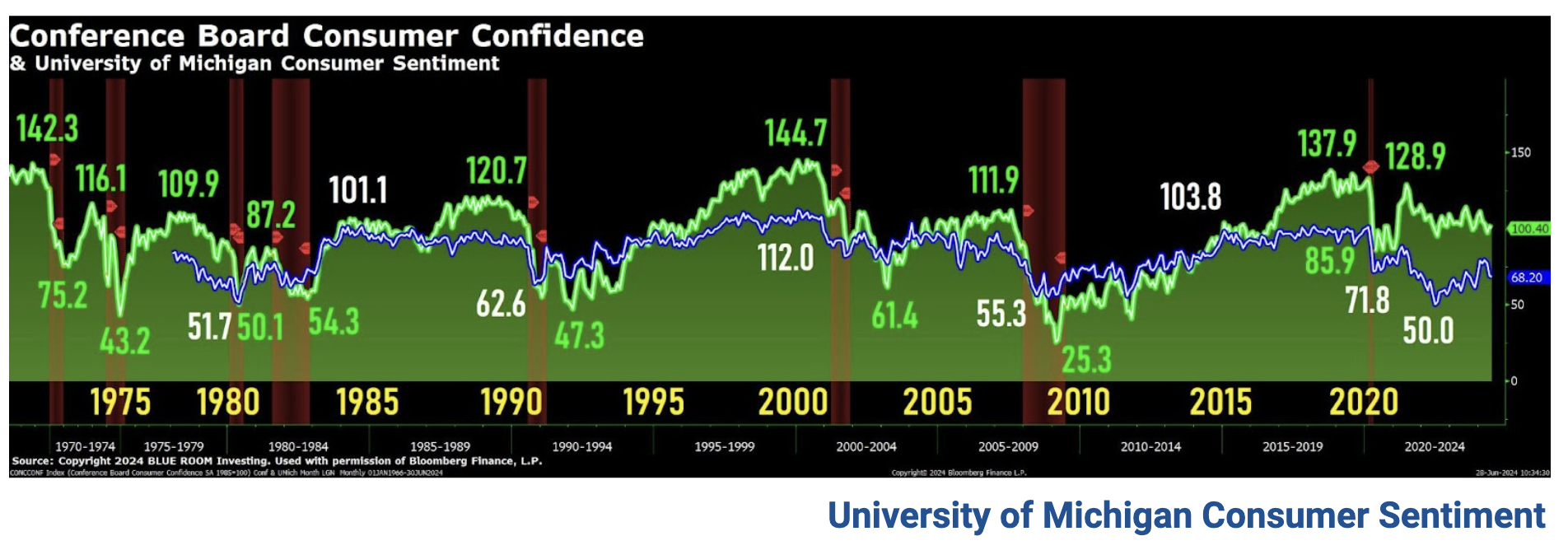

Consumer sentiment held steady at 68.2 in June. This month’s reading was a scant and statistically insignificant 0.9 index points below May and well within the margin of error.

While consumers exhibited confidence that inflation will continue to moderate, many expressed concerns about the effect of high prices and weakening incomes on their personal finances.

These trends offset the improvements in the short- and long-run outlook for business conditions stemming in part from expectations for softening interest rates. Still, sentiment is currently about 36% above the trough seen in June 2022.

All patterns discussed in this report are visible when looking at trends within web interviews alone or phone interviews alone, and thus they are not artifacts of the survey’s methodological transition.

June 27, 2024 BLUE ROOM Meeting 154

Thursday

June 27, 2024

12 PM

Agenda

I. Company Updates

II. Blue Room Investing

III. Blue Room Impact

IV. Icebreaker

Icebreaker Question:

The first Presidential Debate is tonight. If you were President of the United States, what would be your focus?

10% OF ALL BLUE ROOM REVENUES GO DIRECTLY TO FUND OUR NON PROFIT TOGETHERISM.

WE CAN ACCOMPLISH ANYTHING TOGETHER.

These materials do not purport to be all-inclusive or to contain all the information that a prospective investor may desire in considering an investment. These materials are intended merely for preliminary discussion only and may not be relied upon for making any investment decision. Any discussion or information contained in this presentation does not serve as a receipt of, or as a substitute for, personalized investment advice from Blueroom or your advisor.

This publication does not constitute an offer to sell or a solicitation to buy any securities in any fund, market sector, strategy or any other product. Investing is speculative and involves substantial risks (including, the risk of loss of the investor’s entire investment). Past performance is not indicative of future results, and there can be no assurance that the future performance of any specific investment, investment strategy, or product will be profitable.

For more information about us and our general disclosures contact us directly.