Weekend Update #178

Thank you for your continued support and engagement. Each week, we're sharing what companies we're researching and the what, the who and the how that we think makes the companies interesting and unique. This roundup is brought to you weekly by a group of interns, creative minds, artists and investors who believe that through best in class investing along with the democratization of financial education we can do great things together. Enjoy, Explore and Share.

The S&P 500 ended the week above the 5,200 mark, just shy of March 2024’s all-time high, as earnings beats and positive economic growth prospects powered further gains. The outlook for equities is split though, as a 22V Research survey showed 52% and 48% of investors expect the S&P 500’s next 10% move to be higher and lower, respectively. Through this earnings season, 79% of S&P 500 companies beat profit expectations as of last week, yet only 15% of companies beat guidance expectations — the smallest margin since 2020.

Notable companies that reported earnings this week: Affirm, Arm, BioNTech, BP, California Resources, Disney, EOG Resources, Exact Sciences, Instacart, Lyft, Rivian, Robinhood, Shopify, Sweetgreen, Twilio, Uber, Vertex, and Vimeo. A majority of these companies saw muted to negative reactions to results as investors digested company guidance relative to consensus expectations and valuation levels. Sweetgreen saw the biggest move with SG shares ending the week up 43% as in-store design innovations drive operating efficiency and a higher sales outlook.

In economic data for the week, the Fed’s Senior Loan Officers’ Opinion Survey (SLOOS) on Monday showed muted lending activity in response to higher-for-longer interest rates. The percentage of banks considerably tightening lending standards rose to 3.1% in Q1 2024, compared to 1.6% in Q4 2023. Banks somewhat tightening lending standards rose to 15.6% from 12.9%. Demand for commercial & industrial and residential real estate loans continued to contract.

On Wednesday, weekly initial jobless claims surged to 231,000, their highest level since August 2023. It appears to be too early to tell if this trend will persist long enough to prompt the Federal Reserve to cut interest rates, given sticky inflation readings.

Friday’s University of Michigan Consumer Sentiment report for May showed a sharp 13% deterioration in consumers’ current perceptions and future expectations for the U.S. economy, while inflation expectations increased. Deterioration was seen across survey subcategories as well as across demographics, which was enough to grab the market’s attention but will need to be confirmed through alternate sources of data as well as in the University of Michigan’s finalized report later this month.

Although in the FOMC press conference just last week Fed Chair Jerome Powell said, “I don’t see either the ‘stag’ or the ‘flation’, actually,” data points such as Consumer Sentiment have created a chatter in financial news around “stagflation” risks. Per the University of Michigan economists: “The data suggest an increase in downside risks for the economy given the emerging unease across the population regarding multiple facets of the economy.” Inflation and unemployment measures remain at low levels relative to the stagflationary environment throughout the 1970s/80s, but the directional surprises on economists’ estimates of these measures have recently turned negative.

Next week’s economic data will include PPI, CPI, and Retail Sales readings to give further direction for economists’ forecasts. Currently, both the Federal Reserve and most economists are still positive on the U.S. growth outlook for the year as the Fed’s hold on rates allows prices to gradually come back into better balance without a sharp impact to GDP or employment. AI innovation and resilient consumer spending themes continue to power the equity rally and are expected to continue to do so barring sharply negative turns in economic data.

Friday’s Close (Weekly Performance)

S&P 500 5,222.68 (+1.85%)

Nasdaq 16,340.87 (+1.14%)

Dow Jones 39,512.84 (+2.16%)

Thank you Blue Room Analyst JARED FENLEY

ThisAs earnings season began to taper off, the S&P 500 continued its three-week run. Fund One did not fare as well as it was down for the week and trailed the index. Despite this, the Fund continues to be in positive territory for the month. This is highly encouraging as earnings season gives us the opportunity to check in with our entire portfolio and overall, we’re feeling good.

Once again, our biggest winner for the week was newer holding Sweetgreen. After successful option trades earlier in the year, our initial purchase price on the common shares of Sweetgreen was $12.69/share on February 29. On Friday, Sweetgreen reported stronger than expected revenue growth for the first quarter and increased its same store sales forecast for the year to 4-6% from its prior outlook of 3-5%. As a result shares were up 34% on Friday and up 43% for the week. Sweetgreen shares closed at $31.56 which is 2.5x higher than our cost. We remain confident in Sweetgreen for multiple reasons including its approach to robotic technology for salad and bowl assembly and its launch of steak items this week which has taken off nationally. We conducted our own in-house research on the new caramelized steak options at Blue Room HQ and were equally impressed as the market.

On the other side of performance this week was molecular diagnostics holding, Exact Sciences. Exact concentrates in the early detection and prevention of colorectal cancer primarily through its non-invasive stool DNA test, Cologuard. The stock was down 14% over the week after its earnings release which actually beat estimates on revenues but left investors concerned with its growth prospects as it gave disappointing second quarter guidance. Even after reducing our 2024 revenue forecast based on management’s guidance, we continue to believe that Exact Sciences is a solid long term investment. Cologuard remains the industry standard for those who do not need a colonoscopy. In addition, the American Cancer Society is expanding the market by recommending screening for women as well as for people at forty-five years of age. Also, Exact is investing in new cancer screening products which will diversify its portfolio and potentially provide new revenue streams.

Thank you Blue Room Investing President JOHN FENLEY

Executive Summary

Sweetgreen shares are poised to trade higher through 2024 as it continues to not only deliver but also improve on all the right metrics. The company posted Q1 2024 revenue of $157.9 million, a 26% year-over-year increase, while also yielding positive adjusted EBITDA of $0.113 million, which represented 542 basis points of margin expansion. The strong performance was attributable to Same-Store Sales growth of 5% on the back of +5.0% menu price increase and flat transaction volume growth and a 240 basis point decline in labor and related expenses as a percentage of revenue, declining from 31.4% in the prior year period to 29% in the most recent quarter and is positioned to fall further still as the company continues improving how it deploys labor. Raises on revenue, same-store sales and adjusted EBITDA guidance and very positive commentary on the earnings call all helped to propel shares +34% on Friday.

Executive Summary

BioNTech is slowly cementing its position as an oncology company – making its COVID-related past seem like a whimsical detour. As BioNTech’s fiscal performance is heavily skewed to the latter-half of the year, the first quarter earnings call focused more on upcoming catalysts and operational strategies. While BioNTech maintains its infectious disease pipeline – and continues to rake in billions of Euros in annual revenue – its ethos and primary focus lies in its oncology pipeline. Indeed, BioNTech emphasized its role as a “platform-agnostic” oncology company. While mRNA remains the foundation of BioNTech’s technological approach, the company has nearly fully reinvented itself as a compelling large biotech company focused more on developing curative therapies for cancer than one focused on using mRNA to pursue new paths for treatment.

The most significant aspects of the earnings call:

i.) BioNTech reiterated its financial guidance that it set out at its Fourth Quarter and Full-Year 2023 earnings call. Despite the company missing Street estimates on the topline, management quelled any concerns during the call by reinforcing their belief that they are on track to deliver their guidance.

ii.) None of the analysts during the call asked about the company’s COVID franchise; all questions focused on the oncology pipeline, and a few analysts discussed the company’s more exploratory infectious disease candidates.

iii.) BioNTech continues to have a strong financial position, with more than €16.9 billion in total cash plus security investments. In discussing its intention to pursue collaborations to ease the financial burden of clinical trial development, BioNTech emphasized its confidence in having its oncology pipeline carrying the company back to growth and profitability.

EXECUTIVE SUMMARY

Arm is poised to open lower tomorrow at open after the company provided a full year guidance for fiscal 2025 that missed consensus expectations by 1.5% at the midpoint. For the first quarter of 2025, however, revenue guidance was 3.7% better than expected, with greater adoption of Armv9 architecture driving gains. Armv9 is specifically gaining traction with cloud/hyperscale customers and automotive OEMs, augmented by a rebound in global handset market from a CY2023 cyclical low.

In the quarter, Chips reported as shipped were significantly below both BLUE ROOM and consensus expectations, causing royalty revenue per chip to be significantly above our expectations prior to the earnings call. (Consensus estimated royalty revenue “RR” per chip shipped of $0.06; BLUE ROOM estimated RR/chip shipped of $0.065; Arm reported RR/chip shipped of $0.074). (Figure 1)

At first glance this would appear to be driven by a higher contribution of Armv9 architecture than modeled, but the actual case was that Armv9 represented 20.0% of royalty revenues in the quarter (Armv8: ~50.0%; older architectures ~30.0%). Based on a RR/chip shipped estimate of 2x for Armv9 (targeting $0.12 per chip), this translates to about 857 million Armv9 chips shipped and 6.134 billion v8 and older chips shipped. (Figure 2)

By our measure, this means that the RR/legacy chip shipped grew 19.2% in the quarter, and was driven by lower unit contribution from IoT chips, which the company noted are typically high-volume but low value. It may have also been driven by a better-than-expected global handset market in the calendar quarter, leading to higher contribution to mix This would make sense as a majority of units shipped were likely non-premium smartphones. (Figure 3)

Also in the quarter, topline growth was actually primarily driven by a +$60 million increase QoQ in licensing revenue with large contracts signed in the period. (The owners of these contracts were undefined, but it is likely that they are within the client compute, cloud service, and automotive end markets as these are currently the areas of major AI investment). The QoQ increase of $60 million grew above the $22 million estimated by the street, and significantly outpaced BLUE ROOM’s estimate for +$5 million QoQ. We assumed that growth would come from royalties on earlier contracts won for AI.

On company guidance by channel, royalties are expected to grow ~20.0% YoY in 1Q24, driven by Armv9 adoption and a recovery in smartphones. Licensing revenue will grow about +2.0% QoQ (by our measure of “slight” growth) driven by timing/backlog.

For the full year we estimate that royalties can grow ~22.0% and licensing revenue will grow ~41.0%.

Executive Summary

Vertex grew revenue 13.3% year-over-year to $2.69 billion, beating consensus estimates of $2.59 billion, primarily driven by stronger-than-expected TRIKAFTA sales accelerating 18.5% Y/Y. Adjusted EPS grew 12% year-over-year to $4.20, 11 cents higher than consensus. Vertex announced it submitted regulatory marketing applications for the once-daily vanzacaftor triple which was sooner-than-expected, a positive surprise. The company also said its rolling submission for Suzetrigine for acute pain is on track to be completed in the second quarter of 2024. With CASGEVY now improved in most regions and expected to ramp throughout the year, and two potential FDA approvals for additional indications, VRTX shares are poised to gain in 2024 as it successfully diversifies its commercial products beyond cystic fibrosis, and as its R&D pipeline continues to progress.

Executive Summary

Shopify beat on Q1 2024 consensus estimates of revenue growth across Subscription and Merchant segments while beating on adjusted net income, but management guided to a “high teens” growth rate year-over-year for revenue in Q2 2024, which fell short of the consensus $2.005 billion estimate for 19.6% year-over-year growth. This deceleration into Q2 2024 management messaged as a result of lapping the 300-400 basis point impact of the Shopify Logistics business sold in Q2 2023, which will be the last quarter of this impact. Looking at the core business growth ex-Logistics, revenue growth will be low-to-mid 20s growth year-over-year, compared to 29% year-over-year growth in Q1 2024.

Merchant Solutions revenue continues to be powered by GMV growth, which increased 23% year-over-year to $60.9 billion, surpassing the consensus estimate for 20% year-over-year growth. The Merchant Solutions Attach Rate increased quarter-over-quarter to 2.22% of GMV, but continued a downward trend year-over-year falling 2% as Enterprise clients onboarded to the Shopify platform are taking longer than smaller merchants to opt-in to additional tool offerings. The combination is for a still-strong outlook going into the rest of 2024 for Merchant Solutions revenue, especially as Q3 2024 comps get easier as the Logistics sale is lapped.

On the Subscription side, again Shopify will have to lap a pricing increase implemented in Q2 2023, but a Plus Subscription pricing increase will flow through to Q3 and Q4 2024 revenue and margins. Shopify offered Plus merchants to opt into new pricing or sign 3-year contracts at existing prices, so for the next few years, Shopify will have the tailwind of the majority of Plus merchants who opted for long-term contracts while leaving the future benefit of all Plus plans being upgraded to the new pricing. The high opt-in rates seen give management confidence in the value proposition they are offering to Shopify’s biggest clients.

Macroeconomic considerations for the outlook include a weaker consumer spending environment in Europe as well as foreign currency headwinds due to a strong U.S. dollar, while consumer spending in North America remains more resilient. Despite this, Shopify saw the 3rd consecutive quarter of European revenue growing more than 35% year-over-year, and with less than 1% market share in global retail sales, the successes in the North American e-commerce market should translate to international success as well with a long runway for market share growth. The value proposition is especially strong for Shopify’s largest potential clients with recent studies showing a Total Cost of Ownership 35% lower than its competitors.

Executive Summary

EOG shares traded in-line with the broader energy sector despite posting earnings that proved better-than-anticipated on nearly all key measures. Following their Q4 2023 earnings in which they surprised analysts by guiding to higher capital expenditures and lower production estimates, this quarter saw EOG maintain its stance regarding its FY2024 outlook.

The most significant aspects of the earnings call:

(i) EOG had a strong first quarter, with both production and per barrel cash operating costs outperforming both analyst estimates and EOG’s internal estimates.

(ii) When asked about growing consolidation in the Permian, management commented “We're focused on creating shareholder value through the cycles and the consistent way that we've been able to generate that value is through organic exploration. Focus on low-cost operations and a commitment to capital discipline. We have a high level of confidence in our existing portfolio and it's aimed at improving the financial performance of the company.”

(iii) Alongside other major E&P companies, EOG is aiming to transition to a period of consistency – relatively immune from the volatility of the oil market. In their earnings presentation, EOG provided FCF guidance for the next two years that is estimated to increase from 2024 levels even if WTI averages $65/bbl each year.

Executive Summary

Vimeo performed well in the quarter, generating $104.9 million in revenue, beating consensus estimates of $100.3 million by 4.6%. The company achieved positive GAAP operating income and diluted EPS of $2.6 million and $0.04, respectively, compared to consensus estimates of negative profitability in both metrics. Adjusted EBITDA also came in ahead of estimates, with $12.2 million (11.6% margin), compared to $7.5 million for consensus. Bookings grew 0.4% year-over-year to $98.1 million, below estimates of $98.5 million, primarily driven by an accelerated decline in the “Other” segment. With an improved profitability outlook, VMEO shares are poised to gain in 2024 as its Enterprise segment continues to accelerate and become a larger contribution to overall revenue, and its Self-Serve business looks to stabilize and return to growth.

Executive Summary

4D Molecular Therapeutics ended Q1 2024 with $525.9 million in cash and short-term marketable securities with an additional $62.9 million in long-term marketable securities, well above the consensus estimate for $479.7 million. With this, management maintains that the company’s cash runway is into H1 2027, and within that runway, there is ample room to invest into R&D for clinical trial progression as well as SG&A expansion as 4D readies for commercial launches. If the FDA feedback on the 4D-310 Fabry Disease study design with the updated immunosuppressive regimen is positive, there is some potential for the company to achieve commercial sales as early as 2026, but without clarity from the FDA, 4D-150 is expected to be the first product to be commercialized in Wet AMD in 2027. Given the maintained guidance for the Wet AMD Phase 3 trial initiation in Q1 2025, the near-term path to revenue remains clear with an estimated peak funding need in Q1 2028.

4D will have 6 data releases and program updates still to come in 2024, so the company is setting up for a near-term catalyst-rich trajectory.

Catalyst Calendar:

Q2 2024 — 4D-310 Fabry Disease Preclinical NHP Data Submission

Q2 2024 — 4D-175 Geographic Atrophy IND Filing

June 2024 — 4D-710 Cystic Fibrosis Interim Phase 1 Data Update (ECFS)

July 2024 — 4D-150 Wet AMD Population Extension Data Update (ASRS)

Q3 2024 — 4D-150 Wet AMD Phase 3 Clinical Trial Design Update

H2 2024 — Initial interim 4D-150 DME Phase 2 data

H2 2024 — 4D-725 A1AT Deficiency Lung Disease Program Update

H2 2024 — 4D-175 Geographic Atrophy Phase 1 Initiation

H2 2024 — 4D-110 for Chorioderemia & 4D-125 for XLRP Program Update

Q1 2025 — 4D-150 Wet AMD Phase 3 Clinical Trial Initiation

Q1 2025 — 4D-710 Cystic Fibrosis Phase 3 Clinical Trial Initiation

Executive Summary

Editas shares suffered following an earnings call that provided few operational updates and provided little in the way of material financial updates. The stock traded down more than 11% following the earnings release, though regained nearly all of the drop the following trading day. Editas’ key catalyst lies in its mid-year data readout of EDIT-301 for sickle cell disease and beta thalassemia. The company repeatedly mentioned its ongoing conversations with the FDA regarding obtaining a data package for a BLA. Despite positive qualitative signs from Chief Medical Officer Baisong Mei’s interactions with patients, the pending dataset will be a crucible event for the stock as it will determine whether or not the company could achieve commercialization in 2026 – as expected by analysts.

Executive Summary

Exact Sciences beat on revenue estimates in Q1 2024 but came in line with consensus expectations for Q2 2024 revenue guidance. The company also stepped up Q1 2024 OpEx 9.3% year-over-year, which was greater than consensus estimated OpEx growth of 4.4% year-over-year. In Q1 2024, the expense step up comes mainly comes from growth in G&A expenses of 11.9%. On the earnings call, management discussed that they were able to identify higher incremental growth that can be achieved through the addition of sales representatives, so this will drive OpEx growth for the next 3 quarters while G&A sees the most leverage. Operating expense leverage will be seen across every individual category for the full year. The net result is Q1 2024 adjusted EBITDA of $39.2 million, which was a beat on the consensus estimate of $25.7 million when adding back one-time costs, and Exact maintained their guidance range of $325-350 million for the full year.

There are some structural tailwinds that will help power Exact’s revenue growth throughout the rest of 2024 and into 2025. The main factor will be the company lapping the pandemic’s impact on wellness visits and therefore a lower pool of patients available for 3-year rescreens throughout the back half of 2023 and H1 2024. In Q2 2024 alone, 400,000 new patients become eligible for a 3-year rescreen. With health systems integrations increasing to 330 in the quarter, the ease of electronic ordering and direct integration with doctors, in addition to new sales reps, the recurring revenue sales engine should see acceleration of growth. On top of this, management detailed that every ordering cohort since the launch of Cologuard has continued to increase order rates over time. With just 12% market penetration and a growing inability for colonoscopies to meet demand (9-12 month wait times for high-risk patient screening in the case of CEO Kevin Conroy’s wife), Exact is well positioned to see deepened penetration well into the future.

Core Cologuard revenue came in above expectations and reinvestment into OpEx was clearly messaged last quarter, so the results show progress. As guidance implies and management messaged in the call, Exact should be seeing growth from Colorguard rescreenings inflect positively for the last three quarters of the year, reaching 20%+ year-over-year revenue growth in Q3 and Q4 2024.

For the quarter, investors took a fearful reaction to a low Cologuard year-over-year growth number, while management was clear about the high bar for last year’s year-over-year growth due to a mild flu season as well as lapping improvements Exact made to ordering systems last year. The two-year stack comp for revenue in Q1 2024 was 24%, which included both rescreens and the age 45-49 group growing over 40% on a two-year stack and core 50+ aged patients growing over 10%. With the alleviation of competitive concerns around the threat of a liquid biopsy test taking significant market share from Cologuard as well as a significantly higher projected growth rate for Cologuard as Exact moves throughout the year, the company looks to be well-positioned to drive continued growth and operating leverage.

Executive Summary

California Resources Corp. reported earnings that, while positive in many respects, were tainted by one-time charges and non-cash, marked-to-market hedging losses. Production was in-line and upstream revenue surprised to the upside, though a $59 million non-cash hedging loss forced the net revenue figure to miss expectations. Operating expenses were in-line for the most part, though one-time charges forced the net income figure into loss territory. Regarding its guidance, California Resources continues to exclude Aera – and will continue to do so until the merger closes mid-year. Nonetheless, the company slightly revised downward its production guidance, though slightly increased its oil mix as a percentage of overall production. Capital expenditures were adjusted downward to account for the March 2024 Court of Appeals decision in Kern County that limits CRC’s ability to lease new wells.

Executive Summary

Instacart beat on consensus revenue estimates, driven by strength in the Transaction segment and GTV growth of 11.4% YoY compared to the consensus estimate of 9.1% YoY growth. Within this total orders increased strongly at 9% YoY to 72.8 million, which was the highest growth since Q4 2022. Take rate on GTV was 7.25% vs. 7.49% in Q1 2023, but sequentially the take rate was up 15 basis points. Instacart is also achieving this growth with a slightly lower expense profile than previously expected. The net result was $165 million in adj. EBITDA in Q1 2024, which was above consensus estimates of $158 million. Instacart plans to drive this efficient growth into the future, with Q2 2024 guidance of $180-190 million in adj. EBITDA, above the consensus $168 million estimate.

Q2 2024 GTV guidance of $8.0-8.15 billion is in line with prior consensus estimates of $8.063 billion, but with a more significant beat on GTV in Q1, guidance implies deceleration of total order growth going into Q2 2024. This will be the challenge for Instacart through the rest of the year lapping YoY comps that get harder with every quarter throughout the year.

Investments into customer incentives coming out of Instacart’s take rate are paying off with cohort growth in GTV, with management saying the 2024 cohort continues to grow larger than the 2023 cohort. However, management still pointed to declines in GTV among more mature cohorts, which means additional incentive investment didn’t have an effect on reigniting existing customer engagement with the platform. In addition, the cost of revenue is accelerating, faster than revenue, so the additional costs are showing up in various places in the financials.

Advertising revenue growth of 8.5% YoY in Q1 2024 contradicts the +10-15% YoY spend increases cited on BWG calls throughout the quarter, so it appears that active brand partners could still be declining on Instacart. The shareholder letter only cites “over 5,500 active brand

partners”, which could imply YoY deceleration over the past 3 quarters. The theme of ROAS/ad efficiency declines on the platform puts advertising revenue at further risk of deceleration throughout the year.

Overall, Instacart didn’t provide many data points to change the narrative that existing customer engagement is poor, advertisers are finding problems with ads on the platform, and maintaining the Q1 revenue growth rates will be hard to achieve throughout the year. But to the positive side, they are achieving better-than-expected growth with a lower expense profile.

Executive Summary

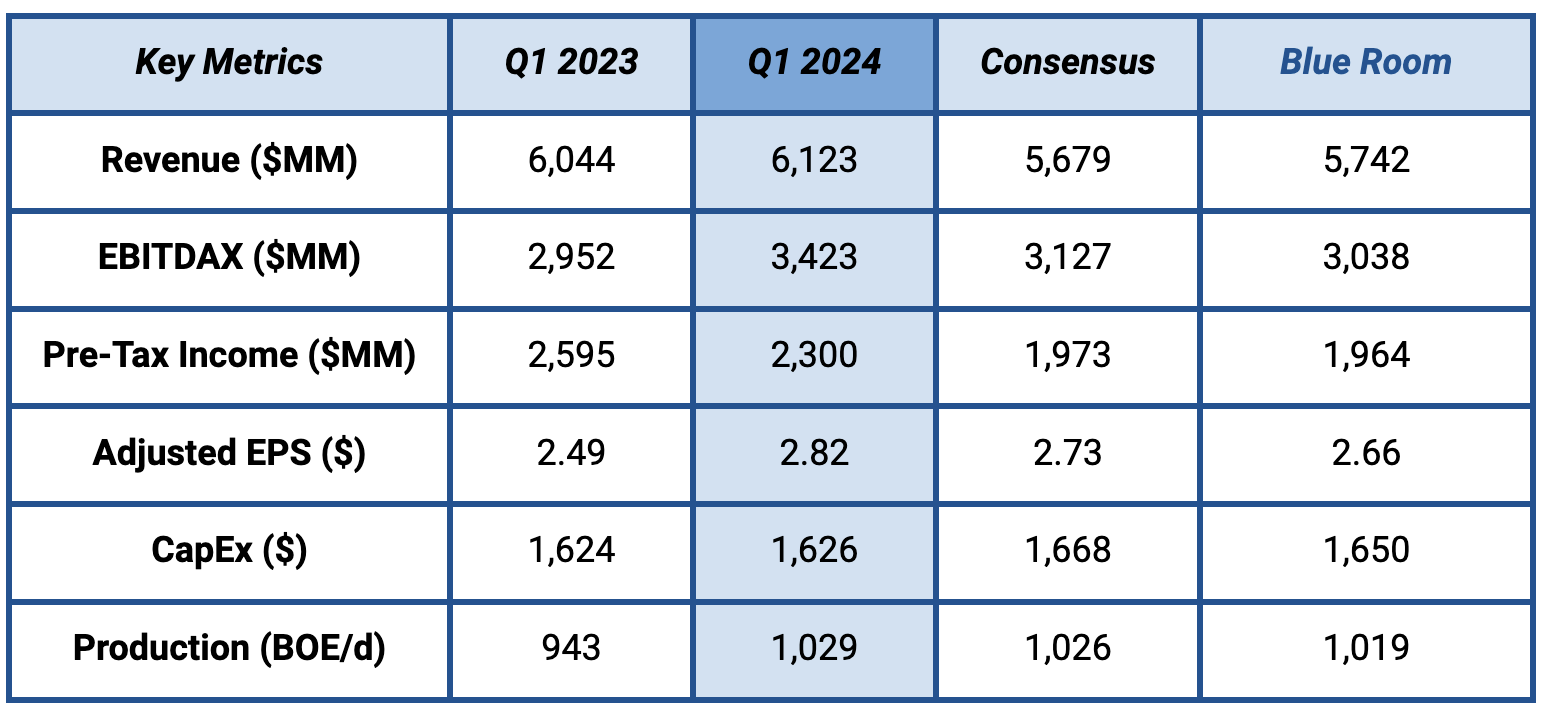

After posting financials that broadly fell in-line with guidance and reiterating their full-year guidance, shares of CPRX are poised to trade flat/in-line with momentum in the short-term, but will trend higher over the medium-term. The launch of Agamree, though talked of highly by management, was not the “wow” factor that some were expecting. While the gross-to-net headwind for Firdapse was less impactful than anticipated, by not outperforming estimates for this quarter, investors will be somewhat dismayed given the excitement that was baked into Agamree’s launch and management not increasing their FY2024 expectations. Catalyst showed decreases in key expense line items including COGS and R&D, but SG&A surprised consensus notably to the upside. Net income was slightly higher than consensus measures, and the company outperformed on adjusted measures.

Consumer sentiment retreated about 13% this May to 67.4 following three consecutive months of very little change. This 10 index-point decline is statistically significant and brings sentiment to its lowest reading in about six months.

This month’s trend in sentiment is characterized by a broad consensus across consumers, with decreases across age, income, and education groups. Consumers in western states exhibited a particularly steep drop.

While consumers had been reserving judgment for the past few months, they now perceive negative developments on a number of dimensions. They expressed worries that inflation, unemployment, and interest rates may all be moving in an unfavorable direction in the year ahead.

All of these patterns are visible when looking at trends within phone interviews alone or web interviews alone, and thus they are not an artifact of the survey’s methodological transition.

10% OF ALL BLUE ROOM REVENUES GO DIRECTLY TO FUND OUR NON PROFIT TOGETHERISM.

WE CAN ACCOMPLISH ANYTHING TOGETHER.

These materials do not purport to be all-inclusive or to contain all the information that a prospective investor may desire in considering an investment. These materials are intended merely for preliminary discussion only and may not be relied upon for making any investment decision. Any discussion or information contained in this presentation does not serve as a receipt of, or as a substitute for, personalized investment advice from Blueroom or your advisor.

This publication does not constitute an offer to sell or a solicitation to buy any securities in any fund, market sector, strategy or any other product. Investing is speculative and involves substantial risks (including, the risk of loss of the investor’s entire investment). Past performance is not indicative of future results, and there can be no assurance that the future performance of any specific investment, investment strategy, or product will be profitable.

For more information about us and our general disclosures contact us directly.