Weekend Update #168

Thank you for your continued support and engagement. Each week, we're sharing what companies we're researching and the what, the who and the how that we think makes the companies interesting and unique. This roundup is brought to you weekly by a group of interns, creative minds, artists and investors who believe that through best in class investing along with the democratization of financial education we can do great things together. Enjoy, Explore and Share.

As we closed out February and turned towards the last month of the first quarter, markets extended the current, start-of-year rally towards new, all-time highs. Reaching the end of another eventful earnings season, market participants saw the Nasdaq and the S&P continue their forceful upward trajectories, breaking through the 16,000 and 5,100 price levels, respectively. The report on Personal Consumption Expenditure defined this week's economic data, leaving a series of questions still to be answered at the Federal Reserves' March meeting. With extensive readouts coming next week on current labor conditions, investors await clarity on the temperature and trajectory of the economy and, most importantly, the Federal Reserve's subsequent appetite for rate cuts.

On February 29, the Bureau of Economic Analysis published data on the Personal Consumption Expenditures Price Index, the Federal Reserve's preferred measure of inflation. Following the Bureau of Labor Statistics publication of the Consumer Price Index on February 13 – which saw above-expectation results for both headline and core at 3.1% and 3.9%, respectively – PCE data this week fell in line with estimates. Headline PCE price increases were measured at 0.34% for the month of January, lowering the 12-month figure to 2.4%. This improvement, while a forceful move towards the Federal Reserve's target rate of 2% and representing the lowest headline PCE level since the first quarter of 2021, also comes after the lapping of January 2023 data, where prices saw a 0.6% increase during the period. On a core basis, PCE rose 0.42% during January, representing the largest increase measured in the last 12 months. Both of these results were driven by high services inflation, continuing the alarms sounded in the mid-February CPI measures.

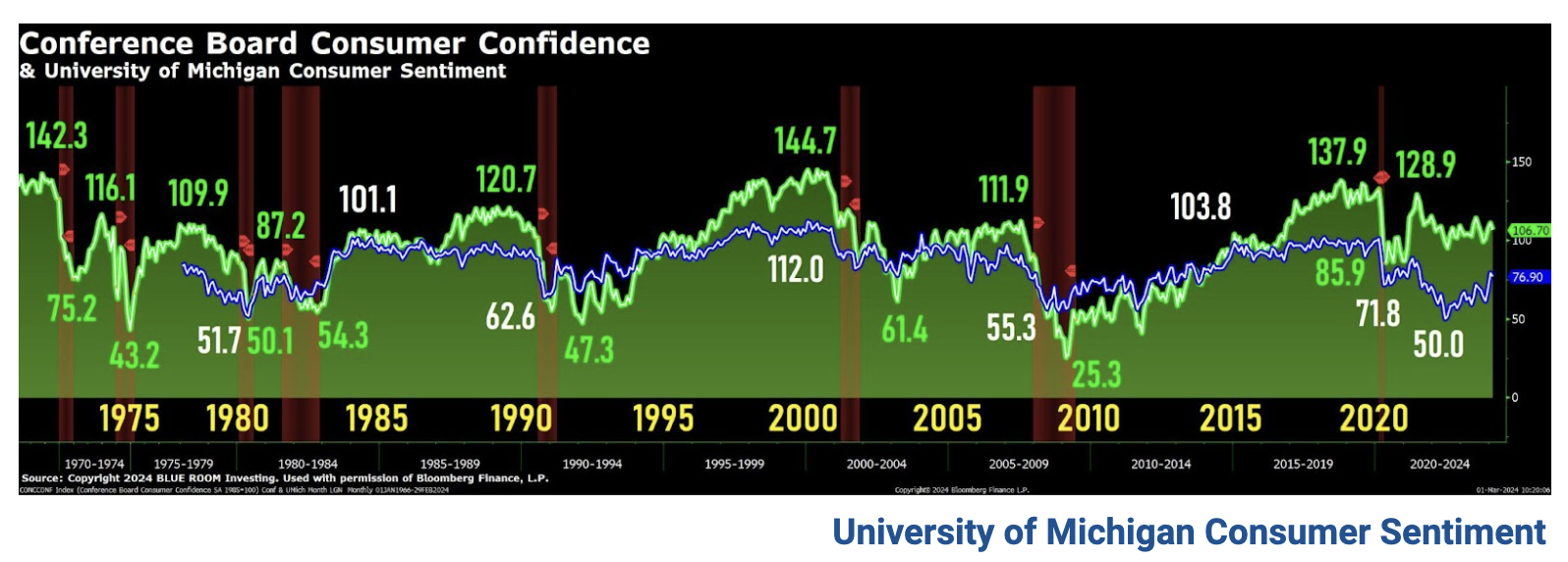

Similarly, on March 1, the University of Michigan published their final survey of consumers for the month of January, outlining a deterioration of sentiment from the previous month and a picking-up of inflation expectations. In the final index, consumer sentiment measured at 76.9 – representing the first month-over-month decline in the last three readings – driven by the increase in one-year inflation expectations to 3.0%. In suite, the percentage of respondents expecting the Federal Reserve to cut interest rates in the next year fell slightly to 35% of consumers. A comprehensive analysis of the University of Michigan Consumer Sentiment survey can be found within the Weekend Update.

Cryptocurrencies continued their impressive run this week, with Bitcoin pushing closer and closer to its all-time high, closing the week at nearly $63,000. Recently-approved Bitcoin ETFs continued to set records for intraday volumes, while spot volumes also reached new highs since the ETF approvals in January.

In Washington, legislatures on both sides of the aisle approved another temporary spending bill in an effort to prevent a partial government shutdown. The bill, engineered by Republican Speaker Mike Johnson, helps to extend funding for agencies including the Department Transportation, the Department of Housing and Urban Development, the Department of Veterans Affairs, the Department of Agriculture, and the Food and Drug Administration. The current package, however, only extends funding at a maximum until March 22, with many agencies only receiving financing for the next week.

Focus on the 2024 election and future national leadership saw even greater acceleration this week as well, with President Biden and former President Trump each making visits to the US-Mexico border. There, each presidential candidate continued to cast the blame for the current immigration crisis on their opponent, with President Biden emphasizing former President Trump's role in influencing the blocking of the Senate's bipartisan border agreement. On the hill, Senate Minority Leader Mitch McConnell announced that he would step down from his post this November after serving in Washington since 1985.

Weekly Performance

S&P 500 5,137.08 +0.87%

Nasdaq 16,274.94 +1.63%

Dow Jones 39,087.38 -0.15%

Thank you Blue Room Analyst AIDAN FETTERLY

Fund One ended a mixed performance week on a high note. We initiated a position in health-focused, fast casual restaurant chain Sweet Green based on Team Leader Omar Guzman’s bullish outlook for earnings. Sweet Green delivered with same store sales growth, new store openings and store level profitability — all exceeding expectations. The stock rewarded shareholders with a 28% move after the earnings report. This move helped offset other portfolio disappointments during the week, including Precision Biosciences ill-timed decision to offer shares at a discount following a recent 52% move post reverse share split. We remain confident in Precision’s long term prospects and look forward to Sweet Green continuing to deliver strong results.

Thank you Blue Room Investing President JOHN FENLEY

Executive Summary

Sweetgreen shares are poised to trade higher through 2024 as it continues to reap the benefits of and build upon the various initiatives it has undertaken, including menu innovation, Infinite Kitchen, and Sweetpass. The company generated 6% of same-store sales growth in Q4 and guided to 3-5% in 2024, due in part to their launch of Protein Plates in October of last year. Sweetgreen grew restaurant-level profit margins by 270 basis points to 17.5% in 2023 and guided to further expansion of 105 to 205 basis points in 2024, while also indicating they have a "clear path to 20%-plus" from Infinite Kitchen, which will add "at least 7 points of margin improvement" from the current 17.5% level in new stores and retrofits, implying an expected long-term restaurant-level margin of at least 24.5%.

Executive Summary

Prior to the earnings call, BLUE ROOM forecasted a directionally positive reaction to Ambarella’s fourth quarter results, predicated on guidance that aligned with current street estimate for modest growth in FY2025. We believe this benchmark was achieved after the results were reported. According to CEO Dr. Fermi Wang, both Automotive and IoT business segments are expected to grow out of cyclical lows and into secular growth trends based on the company’s AI solutions. The CV2 family of AI-SoCs will be the largest driver of revenue in the first half of FY2025, with an expectation for CV5 SoC shipments to double year over year for the full year. Volume for CV5 is currently portioned to the IoT business, but management expects automotive OEMs to go into production in the second half of the fiscal year. Based on the Executive’s comments, we continue to expect the recovery to be back half weighted, as CV5 SoCs carry a premium ASP relative to prior generation CV2s. We re-emphasize the doubling of CV5 five nanometer shipments in 2025, as it is a leading indicator of the capacity growth and scaling that the company can do in the 5nm node, which is of particular significance given CV3 will launch at 5nm nodes.

Growth for Amabrella’s CV-SoC business has been mostly led by the IoT segment as global end-demand for these products has a more mature market, but Ambarella is finding particular success in China with its CV72AQ automotive solution. It is now widely understood that China’s transition to more autonomous, more electric, vehicles is scaling much faster than it is in the U.S., so Ambarella’s adoption in the region is a good precursor to global adoption in future periods.

Lastly, the N1 processor for edge-inference appears to need no further development capacity as a large portion of the algorithms Ambarella has already worked on for CV3 (computer vision and deep learning) translated smoothly into the development of the inference processor. For now, the N1 chip still sounds like more of a science experiment rather than a product catalyst, but revenue from this edge-inference device will be additive to Ambarella’s existing AIoT SAM.

Nvidia in 2024 Is Everything the Yahoo! of 2000 Wished to Be.

Executive Summary

Zuora grew subscription revenue 11.9% year-over-year to $100.2 million, above consensus estimates of $99.8 million. The company also generated $15.9 million in adjusted operating income, ahead of consensus’ $12.4 million estimate, producing a margin of 14.3%. Adjusted EPS was $0.12, more than double the $0.05 estimate. While Q4 results were positive, the company experienced churn from two large customers that had a negative impact on FY2025 annual recurring revenue and dollar-based retention rate. Due to the unexpected churn, Zuora’s guidance of 7-8% year-over-year growth in subscription revenue came in lower than analysts’ expectations of 10.5%. However, guidance on profitability metrics came in well above street expectations as the company continues to improve operational efficiency. Despite the challenging macro environment, the company is executing its plan for faster installs as it acquired 40% more logos in Q4 compared to the previous year and it closed deals 25% faster in FY24 compared to FY23. ZUO shares are likely to remain range bound in the near-term with potential to appreciate in the second half of 2024 as the company gets better visibility with its large enterprise customers.

Consumer sentiment moved sideways this month at 76.9, slipping just two index points below January and holding the gains in sentiment seen over the past three months.

Expected business conditions remained substantially higher than last autumn, with short-run expectations now 63% above and long-run expectations 46% above November 2023 readings.

For all but one index component, readings this month were higher than all values between mid-2021 and the end of 2023.

Consumers perceived few changes in the state of the economy since the start of the new year, and they appear to be assured that inflation will continue on a favorable trajectory.

Sentiment is currently 8 points shy of the historical average since 1978.

Median One-Year and Long-Term Inflation Expectation Rates

The median expectation for one-year inflation (blue line) increased to 3.0%.

The median expectation for long-term inflation (green line) remained unchanged at 2.9%.

Year-ahead inflation inched up from 2.9% in January to 3.0% in February. For the second straight month, short-run inflation expectations have fallen within the 2.3-3.0% range seen in 2018 and 2019. Long-run inflation expectations remained at 2.9% for the third straight month, staying within the narrow 2.9-3.1% range for 28 of the last 31 months. Long-run inflation expectations were modestly elevated relative to the 2.2-2.6% range seen in the two years pre-pandemic.

Executive Summary

On February 27, Beam provided their fourth quarter and year end financial results for 2023. As has been the case, Beam Therapeutics elected not to hold an earnings call to discuss their operational and financial highlights. All key information – excluding income statement data – that Beam highlighted in their press release was previously shared by the company when they presented at the JP Morgan Healthcare Conference on January 8, 2024.

Summary

Workday reported a solid Q4 with top earnings beat expectations to close a strong fiscal year 2024. Subscription revenue grew 17.7% year-over-year to $1.76 billion, contributing ~92% to total revenue and non-GAAP operating margin was ~24%. Full year subscriptions grew 18.6% year-over-year, total revenue grew 16.8% year-over-year, and non-GAAP operating margin improved to 24%, up 450 basis points.

Workday entered fiscal year FY’25 well positioned to deliver another year of durable subscription revenue growth coupled with expanding margins. Subscription is expected to grow 18.5% for Q1 FY’25, and grow 17% - 18% for full year FY’25. Total revenue is expected to grow 15% - 16% for FY’25 and non-GAAP operating margin is expected to improve 50 basis points to 24.5%. The company expects to generate operating cash flow of $2.25 billion for FY’25.

The company officially named Carl Eschenbach CEO effective February 1, 2024. Aneel Bhusri remains integral to the organization as co-founder and as executive chair. Some management positions are appointed, aiming to innovate products and grow the international market.

To further accelerate the AI roadmap, Workday announced an agreement to acquire HiredScore which provides AI-powered talent orchestration solutions to help improve recruiting and internal mobility processes.

In their upcoming R1 release, many of the generative AI use cases showcase it rising will be put into the hands of early adopters, including job descriptions and knowledge articles.

The Board of Directors approved a new share repurchase program, with a term of 18 months, to repurchase up to an additional $500 million of shares of its Class A common stock.

2024

THE YEAR OF

— AND —

This is the year of AND.

…

The rigor at Blue Room is mind-blowing.

The analyst team arrives between 5:30 and 7:30am every day. Everyone looks sharp, spry and attacks the day. At 7am every Monday morning, the team meets with our Vietnam office. At 9:30am, the daily bullpen starts like clock-work connecting the team to discuss our holdings, the market, geo-political implications, the economy and any daily triggers that could affect any of the above. At noon every Thursday, the entire Blue Room network connects globally — our vital impact companies, partners and muses. Every Friday, the team heads out for our weekly out-of-office lunch at Smokin’ Yards BBQ. Every Saturday morning at 6am MST, we publish the Weekend Update where the team galvanizes around research and thought-leadership pieces they have been working on all week. Monthly, we hit the Economic Club of Colorado for inspiring speakers and networking with the local economic community. Seasonally, we head to the Museum of Contemporary Art for an event or opening. Biannually, we host events at Blue Room for our clients, partners, community, family and friends.

I guess what I am trying to express is that at Blue Room, we have figured out how to operate as a unit with discipline, effiiciency, innovation and community engagement.

Now, how can each and every one of us make more of an impact?

Impact on work, impact on culture, impact on the community, impact in the way we conduct ourselves.

AND

is the difference.

Between showing up AND engaging meaningfully.

You do superlative work AND then you go farther.

AND is not just doing what you did the day before.

AND is thinking of the way to make it more.

AND sets energy in motion, it will be the difference as we prove that >>>

Through best-in-class investing, we seek to make the world a better place.

-Blue Room Mission.

We took some time away from the screens to get our hands dirty and dive into the intention..

As an homage to this 2024 focus at Blue Room, the investment team created art pieces pushing the wonder of AND / &.

Ian Carter, Analyst

Omar Guzman, Team Leader

Aidan Fetterly, Analyst

Nick Peart, Analyst

Naia Morse, Director of Impact

Spencer Wootten, Analyst

Jim Chomas, CFO / President

Eli Haynes, Director of Investor Relations

Nina Sohn, Director of Community Engagement

Jared Fenley, Analyst

STAY TUNED FOR UPDATES FROM

THE YEAR OF

—AND—

Executive Summary

Last quarter, Best Buy lowered its S.S.S. outlook for the full year by 150 bps. Actual comparable sales results fell lower by 5 bps, but the company was able to beat the 4.05% implied midpoint of adjusted operating margin by 5 bps. The quarter was all about omnichannel efficiency, which Best Buy will need to lean on as margins remain below trend during a downcycle in the CE industry. Regarding the shape of revenue throughout the quarter, November was down 5%, December was down 2%, and January was down 12%. We were pleasantly surprised with the stock’s reaction (+1.51% D/D), but expect negative sentiment to put pressure on the equity due to lower FY2025 sales guidance than expected. We model YoY pressure coming in all categories except Services and Computing & Mobile Phones, based on the expectation that AI will drive desire for upgrades as we begin to enter the refresh cycle that Corie Barry estimates is every 3 to 7 years.

In recent quarters, Best Buy benefitted from favorable product margins as they lapped inflationary headwinds in calendar ‘21/’22, but this is beginning to reverse as management reported unfavorable product margins in the fourth quarter. This was slightly offset by the higher rates memberships and Health initiatives pulled in for the quarter (responsible for the 60 bps increase in margin rate YoY).

Management reported closing 24 stores in F24, while opening 11 in the period. Moving forward the company will continue to invest in international opportunities, spending less CAPEX in F25. Instead, the company will focus on refreshes and new locations in geographies where Best Buy has not operated before.

No update on consumer demographics:

Ended the quarter with 7 million My Best Buy memberships (49.99 to 179.99 per year); membership dropped free installs so margins are going up on memberships

Shopping patterns more normalized to pre-pandemic; December start was a lull but there was strong demand in the four days before Christmas

Executive Summary

On February 28, California Resources Corporation (CRC) held an analyst call to discuss their 2023 fourth quarter and full-year earnings. CRC updated investors on its high-level earnings expectations on January 4, and provided further information when it announced its acquisition of Aera on February 7. CRC’s guidance was relatively opaque, as they are hesitant to provide any figures inclusive of Aera until the acquisition closes in the second half of the year. Further, their CapEx and production guidance is conditional on whether or not the company can get approvals for further production – as California’s state government has been adamant about decarbonizing. The analyst’s questions focused primarily on the ability to secure permits alongside progress related to carbon storage and sequestration.

Executive Summary

4D Molecular Therapeutics reported $288.2 million in cash at the end of 2023, above the consensus estimate for $266.7 million — and an extension of the company’s cash runway into H1 2027, up from the prior guidance of H1 2026 in January 2024 prior to the $281 million offering. This is a big step forward for the cash runway. 4D did step up on R&D and G&A expenses slightly, but the additional cash runway provides some room for additional investment now. Other pipeline highlights underline the progress 4D is making, widely as expected. One milestone change of note is the 4D-150 Phase 2 DME data readout was pushed back from H1 2024 to H2 2024.

Thursday

February 29, 2024

12 PM

__________

Hello Blue Room,

Please join us for a special global meeting -

February 29.

Leap Year!

Agenda

I. Blue Room Investing

II. Blue Room Impact

III. Icebreaker Question: Leap Year 2024

Open prompt for your stream of consciousness when inspired to think about a day which comes along only every four years.

Executive Summary

Editas shares exploded following its earnings call on February 28 when the company announced that its clinical trial for reni-cel – its lead portfolio candidate – will act as a single Phase 1/2/3 trial, greatly expediting the timing required for a BLA. Editas plans to readout data from the RUBY trial mid-year with a patient population of at least 18. In addition to its lead candidates for sickle cell disease and beta thalassemia, Editas hopes to establish preclinical proof of concept for an in vivo therapeutic this year in an undisclosed location.

Executive Summary

The story of Guardant’s Q4 2023 earnings is strong execution on their core business but clouded by a push back in the expected Shield FDA approval from H1 2024 to H2 2024 as the FDA works to fill panel advisory seats with the needed personnel at their end. The review meeting is now expected to occur in late Q2 2024. In addition, there are lingering competitive concerns around Shield’s CRC positioning given the low (13%) advanced adenoma sensitivity, and the true competitive advantage Guardant is working to by adding on lung, breast, bladder, and pancreatic indications to the Shield blood test are too far in the future to have a clear path to valuation implications in the near-term.

Guardant Health beat on revenue and adjusted profitability metrics in Q4 2023 but guided the midpoint of FY 2024 sales and cash burn below consensus expectations. Similar to Exact, Guardant has been growing precision oncology revenue at a strong pace, with 31% YoY growth in FY 2023, accelerating from 29% YoY growth in 2022, but although the company probably expects to deliver FY 2024 sales at where consensus expectations were coming into the call, they guided to that as the top end of guidance in order to be able to beat expectations throughout the year. One caveat with guidance is Guardant is only baking in core precision oncology revenue, without expected contribution from initial Shield tests, so any Shield performance throughout the year only represents upside for the year.

On the cash levels and burn side of the financials, 2/3 of the $325 million expected FY 2024 cash burn is slotted to come on the screening side of the business while 1/3 still comes from MRD tests — as Guardant’s new Response, Reveal, and TissueNext tests all need to see steps up in reimbursement to become gross margin positive for the business. Guardant is also guiding to having enough cash on hand with $1.2 billion to last until the full company achieves free cash flow positivity in 2028 and comes as Guardant reaches free cash flow positivity on the precision oncology side of the business in 2024.

The most interesting parts of the investor call were Co-CEO AmirAli Talasaz’s comments on the USPSTF’s consideration of adherence rates for the upcoming 2026 review and his acceptance that management should have managed expectations better going into Shield. He went as far as to say if regulation doesn’t align that they will discontinue the Shield tests so as to not burn excessive cash — coming directly from the head of screening. It would take beyond 2026 USPSTF review for Guardant to make that decision, but as the precision oncology side of the business is already cash flow positive, this would be an interesting outcome for the business. Another way of looking at this is that, even if reimbursement comes in low for Shield, USPSTF classifies it as a second-line test, and Freenome’s results do not far surpass Shield’s, any single catalyst to the positive remains as upside for Guardant’s valuation.

However, given the weight of the Freenome results priced into the current valuation, there is a significant risk in the event that Freenome’s AA rate comes in at 25% sensitivity or higher given current levels of Shield investment would make a drop on future Shield sales estimates have a significant negative impact on valuation.

Executive Summary

EOG shares traded down on Friday after exceeding analyst expectations for capital expenditures and providing production forecasts that were lower than anticipated. EOG forecasted 2024 capital expenditures between $6.0 and $6.4 billion, compared to estimates of $6.04 billion. EOG also mildly missed Adjusted EPS figures slightly despite beating on GAAP measures across the income statement. Following the call, four analysts cut their price targets by an average of 5.5%, but no analysts changed their investment recommendations.

SDGR: Schrödinger

Q4 2023 Earnings Review

by Jared Fenley

Executive Summary

Rocket provided a significant $100 million cash balance beat on consensus expectations in Q4 2023, with an unexpected positive cash inflow of ~$20 million during the quarter on top of prior cash flow trends and the better-than-expected operating leverage. The result is an updated projected cash runway to “into 2026” from “through 2025” previously. Key pieces of information included that investors were looking to hear is the Kresaldi PDUFA date remains on track for June 30, 2024, the BLA and MAA applications remain on track for H1 2024 submission, and the Danon Disease Phase 2 program continues to progress. Outside of the positive cash news, the press release is short and sweet with no big announcements.

Executive Summary

Intellia Therapeutics continues to progress towards its stated goal of achieving a BLA for its lead product candidate NTLA-2001 in 2026. In the first quarter of 2024, Intellia aims to dose the first patient in the pivotal Phase 3 MAGNITUDE trial for ATTR-CM. MAGNITUDE aims to enroll 765 participants. In addition to NTLA-2001 for ATTR, Intellia continues to progress on its other candidates. The company aims to initiate a Phase 3 study for NTLA-2002 in the second half of 2024 and dose the first patient in a Phase 1 study of NTLA-3001 by year-end.

Executive Summary

Schrödinger provided a beat on software revenue in Q4 2023, but the singing of the 3-year Eli Lilly & Co. expanded partnership leaves a tough comp for the company to lap in 2024 and 2025. There were changes to management’s guidance methodology for the upcoming year with internally lowered probabilities of signing new multi-year software contracts in Q4 2024 as well as lower probabilities for the estimated timing of partners’ development programs that would trigger larger milestone payments to Schrödinger. The third change is Schrödinger is no longer incorporating the probability of new collaborations in the period to drug discovery revenue. So although there are a multitude of opportunities for Schrödinger to sign important contracts or for a partner to trigger payments to the company in the next year, Schrödinger’s conservative guidance methodology provides a high-probability outcome without adding back positive catalyst potential. This has the effect of bringing down revenue and earnings estimates in the near term but will provide upside surprise in the case that these low-visibility events do occur.

In addition, the lumpiness that multi-year software contract signing implies for revenue makes Schrödinger’s trajectory harder for consensus to model, in which case, there are sharp reactions to changes in revenue growth despite a trend toward 2 to 3 year software cycles if larger customers continue shifting to that payment model.

Schrödinger is excited to provide clinical data from its first MALT1 and CDC7 programs in late 2024 or 2025 as well as submit the Wee1/Myt1 IND this year and a 4th IND in 2025 — all of which will be concrete data points, which provide opportunities to validate the magnitude of impact of large-scale deployment of Schrödinger’s software on discovery programs. However, as the pipeline will be modeled more like an early-stage biotechnology company until Schrödinger can sell or partner those assets, the drug discovery investment side of the business also has low visibility for investors at this point.

In sum, Schrödinger demonstrated strong 50% growth in the number of software customers spending more than $1 million per year on software — growing from 18 to 27 in 2023 — but near-term revenue numbers will be clouded by low visibility into the timing of large software customer contract renewal sizes as well as a much more conservative guidance range on the drug discovery part of the business. As small biotechnology companies are struggling with their own capitalization levels, the business will at the same time have to lap the large flow of small software customers that contributed to demand in 2020-2021.

Executive Summary

WeightWatchers shares are set to continue to trend downwards as the company continues to disappoint on KPIs, financial data, and suffers from the loss of key personnel. WW missed estimates on a slew of income statement items and posted disappointing guidance in most key items – excluding Clinical users, which topped estimates. In the earnings call, management was on their heels and seemed defensive. They kept discussing the future and failed to mention as much data from the past quarter as they had in the past – especially numbers related to churn. Furthermore, Oprah Winfrey announced that she is stepping down from the Board and is donating her shares to the National Museum of African American History and Culture.

Summary

Zoom reported a stronger Q4 result than expected to finish fiscal year FY24, with total revenue coming in at $1.146 billion, up 3% year-over-year. In which, enterprise revenue grew 5% year-over-year, representing 58% of total revenue and online business showed some sign of stabilization with average monthly churn rate remaining at 3% as last quarter. Non-GAAP income grew by 10% year over year to $444 million, representing 38.7% margin.

Operating cash flow and free cash flow margins expanded to 30.6% and 29%, respectively. Zoom ended the quarter with approximately $7 billion in cash and cash equivalents, allowing Zoom the flexibility to consider M&A options to accelerate growth.

Entering fiscal year FY’25 with a prudent outlook, Zoom expects its total revenue to be approximately $4.6 billion, up 1.6% year-over-year growth. Q2 is seen as the low point from a year-over-year growth perspective and to accelerate from there. Non-GAAP operating margin is expected to be approximately 37.5%. The board has authorized a $1.5 billion share repurchase program starting execution this quarter.

The growth being driven by Zoom Phone, by Zoom Contact Center, which continue to mature by the effect that AI and adoption of Team Chat are having on the overall retention metrics of a company. Zoom is seeing more and more medium and large customers adopt Zoom Contact Center. Contact Center suite is beginning to win in head-to-head competition with legacy incumbents.

In terms of Zoom’s product innovation, the base product includes AI Companion and their newly launched tiered pricing allows customers to add specialized CX capabilities such as AI Expert Assist, workforce management, quality management, virtual agent, and omnichannel support.

10% OF ALL BLUE ROOM REVENUES GO DIRECTLY TO FUND OUR NON PROFIT TOGETHERISM.

WE CAN ACCOMPLISH ANYTHING TOGETHER.

These materials do not purport to be all-inclusive or to contain all the information that a prospective investor may desire in considering an investment. These materials are intended merely for preliminary discussion only and may not be relied upon for making any investment decision. Any discussion or information contained in this presentation does not serve as a receipt of, or as a substitute for, personalized investment advice from Blueroom or your advisor.

This publication does not constitute an offer to sell or a solicitation to buy any securities in any fund, market sector, strategy or any other product. Investing is speculative and involves substantial risks (including, the risk of loss of the investor’s entire investment). Past performance is not indicative of future results, and there can be no assurance that the future performance of any specific investment, investment strategy, or product will be profitable.

For more information about us and our general disclosures contact us directly.