Weekend Update #164

Thank you for your continued support and engagement. Each week, we're sharing what companies we're researching and the what, the who and the how that we think makes the companies interesting and unique. This roundup is brought to you weekly by a group of interns, creative minds, artists and investors who believe that through best in class investing along with the democratization of financial education we can do great things together. Enjoy, Explore and Share.

Entering the week, swaps traders priced in 50:50 odds of a March cut in Fed rates and marked a notable step-down from 75% chance at the start of the year. Adding to the rate speculation dynamic were the cuts to the US Treasury’s quarterly borrowing estimate to $760. On a corporate level, Amazon.com Inc abandoned its planned $1.4 billion acquisition of iRobot.

On Tuesday, the Consumer Confidence Index rose nearly 7 points to 114.8, the highest reading in the measure since December of 2021. JOLTS data showed job openings increased against economist estimates for a decrease. Key market leaders Alphabet and Microsoft reported with Google reporting search advertising revenue that came in below consensus while Microsoft grew at a strong pace in the quarter. AMD upwardly revised its full year sales of its AI Chips from $2.0 billion to $3.5 billion. On Wednesday, the FOMC held rates steady at 5.25% - 5.50% and markets got a frank indication of the likelihood of a March rate cut after Fed Chair Jerome Powell said that he didn’t think that March rate cuts were likely. He also noted that the Fed was looking to be more ‘confident’ that inflation is at, and will remain at 2.0%. Stocks rose at the onset of the meeting but quickly fell to session lows after Powell’s comments. On Thursday, Initial and Continuing Claims came in higher than expected and higher than the prior week’s readings, alluding to potentially looser labor markets. The figures were a two-month high. Facebook parent Meta and Amazon outperformed into session close while Apple’s China headwinds put pressure on the equity. Finally, to end the week Nonfarm Payrolls added a whopping 353k jobs, which was welcomed as a sign of economic durability, in stark contrast to the prior negative implications of strong labor data over the past several months. Powell noted that growth and productivity were no longer primary concerns to upward inflationary pressure, given the dynamic of outsized GDP growth and lower inflation in 2023.

Ultimately, markets were relatively on edge going into the middle of the week as some thought that an earnings collapse in big tech and Powell’s comments toward the March rate cut bet would drive markets lower, but economic data complemented overall dovish Fed commentary and markets found a way to push ahead for the week.

Weekly Index Performance

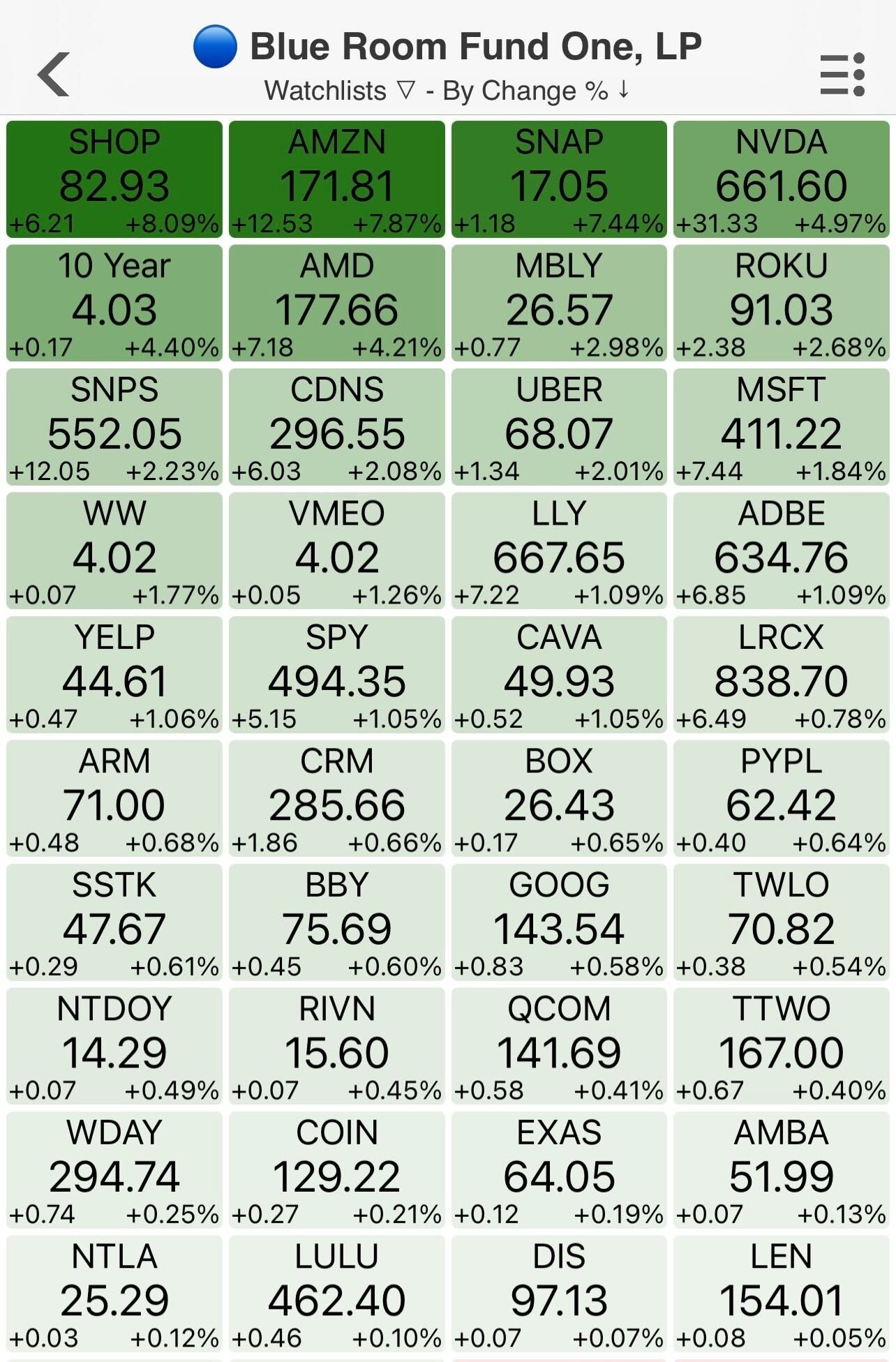

S&P 500 4,958.61 +1.38%

DJIA 38,654.42 +1.43%

Nasdaq 15,628.95 +1.12%

Key Economic Readings Next Week

Monday February 5th — S&P Global US Services & Composite PMI

Wednesday February 7th — MBA Mortgage Applications & Trade Balance

Thursday February 8th — Initial Jobless Claims & Continuing Claims

Thank you Blue Room Analyst IAN CARTER

Operator

Good day, and welcome to the Apple Q1 Fiscal Year 2024 Earnings Conference Call. Today's call is being recorded. At this time, for opening remarks and introductions. I would like to turn the call over to Suhasini Chandramouli, Director of Investor Relations. Please go ahead.

Suhasini Chandramouli

Thank you for joining us. Speaking first today is Apple's CEO, Tim Cook; and he'll be followed by CFO, Luca Maestri. After that, we'll open the call to questions from analysts.

Before turning the call over to Tim, I would like to remind everyone that the quarter we're reporting today included 13 weeks, whereas the quarter we reported a year ago included 14 weeks.

Please note that some of the information you'll hear during our discussion today will consist of forward-looking statements, including, without limitation, those regarding revenue, gross margin, operating expenses, other income and expense, taxes, capital allocation and future business outlook, including the potential impact of macroeconomic conditions on the company's business and results of operations. These statements involve risks and uncertainties that may cause actual results or trends to differ materially from our forecast. For more information, please refer to the risk factors discussed in Apple's most recently filed annual report on Form 10-K and the form 8-K filed with the SEC today along with the associated press release. Apple assumes no obligation to update any forward-looking statements, which speak only as of the date they are made.

I'd now like to turn the call over to Tim for introductory remarks.

Tim Cook

Thank you. Suhasini. Good afternoon, everyone, and thanks for joining the call. Today, Apple is reporting revenue of $119.6 billion for the December quarter, up 2% from a year ago despite having one less week in the quarter. EPS was $2.18, up 16% from a year ago and an all-time record.

We achieved revenue records across more than two dozen countries and regions including all-time records in Europe and rest of Asia-Pacific. We also continue to see strong double-digit growth in many emerging markets with all-time records in Malaysia, Mexico, The Philippines, Poland, and Turkey, as well as December quarter records in India, Indonesia, Saudi Arabia, and Chile.

In Services, we set an all-time revenue record with paid subscriptions growing double-digits year-over-year. And I'm pleased to announce today that we have set a new record for our installed base, which has now surpassed 2.2 billion active devices. We are announcing these results on the eve of what is sure to be a historic day as we enter the era of spatial computing.

Starting tomorrow, Apple Vision Pro, the most advanced personal electronics device ever, will be available in Apple stores for customers in the U.S. with expansion to other countries later this year. Apple Vision Pro is a revolutionary device built on decades of Apple innovation and it's years ahead of anything else. Apple Vision Pro has a groundbreaking new input system and thousands of innovations, and it will unlock incredible experiences for users and developers that are simply not possible on any other device.

We forecast AMD to get support from buyers that are bullish on the revised Mi300 revenue forecast for the full year, despite feeling pressure in other segments of the business. The company updated its Mi300 AI accelerator forecast from $2 billion to $3.5 billion, which fell below BLUE ROOM expectations, as we had modeled over $5 billion in revenue for the product category. Despite the success AMD has seen with its go-to-market in data center AI, its sequential Data Center growth is far behind its leading competitor and questions the market’s view on AMD’s near-term growth prospects in this end-market. Even if we remove the EPYC CPU revenue, $290 million in sequential dollar growth in the quarter which would compare to the consensus forecast for $2.1 billion in Q/Q for Nvidia. On a unit basis, this would appear to display a significant disparity between system adoption. We do, however, remain bullish on AMD as a second line data center GPU supplier and regard its data center CPU business having strong product tailwinds after gaining share against Intel in the quarter.

Additionally, for the first quarter of 2024, AMD expects 1Q24 total revenue to be approximately $5.4 billion, plus or minus $300 million, which misses consensus of $5.8 billion by ~7% at the midpoint.

Sequentially AMD expects:

Data Center Segment revenue to be flat to the 4Q24 revenue figure of $2.28 billion, with a seasonal decline in server sales offset by a strong Data Center GPU ramp.

This was roughly in-line with the consensus expectation for $2.24 billion.

Client, Embedded and Gaming segments are expected to decline sequentially, with semi-custom revenue expected to decline by a significant double-digit percentage.

While the forecast was roughly in line with consensus, the Gaming segment is guided to decline more than expected.

In the opening month of 2024, crude oil prices remained relatively subdued despite growing geopolitical tensions and continued economic strength. The West Texas Intermediate benchmark started the year at $71.64/barrel and finished up 1.92%, ending the month at $73.03/barrel – continuing to trade on the lower side of its channel between $70 and $80/bbl. If January is indicative of what is to come this year, the outlook for oil is relatively bearish, as in the face of heightened geopolitical risks and hawkishness on the part of Saudi Arabia, crude oil prices only increased marginally – reaching a local peak for the month at $75/bbl.

The month began with Saudi Arabia attempting to bolster prices by quelling concerns surrounding fracture within OPEC. On January 2, OPEC released a statement demonstrating its commitment to unity following Angola’s departure from the producer group. The press release began “At the outset of 2024, the OPEC Secretariat in consultation with OPEC Member Countries and the non-OPEC producing countries participating in the Declaration of Cooperation (DOC), re-affirms the full commitment by the countries participating in the DoC to unity and cohesion, as well as their continued and unwavering efforts to maintain oil market stability going forward through the Declaration of Cooperation, signed on 10 December 2016 and further endorsed in subsequent meetings.” The press release continued: “The unprecedented levels of cooperation, dialogue, mutual respect and trust will continue to be the basis for these continued collaborative efforts going forward. This is for the benefit of all producers, consumers and investors, as well as the global economy at large.” While the risks of smaller producer states leaving OPEC remain, the likelihood of a larger member of OPEC leaving the producer group remains incredibly low. Indeed, concerns of the band breaking up have subdued.

Consumer sentiment confirmed its early-month reading, surging 13% to 79.0 — its highest level since July 2021 — reflecting improvements in the outlook for both inflation and personal incomes. January's gain has been exceeded only five times since 1978, one of which was last month at an even larger increase of 14%.

Consumers expressed gains in their views on their personal finances as well as the macroeconomy — The short-run business outlook soared 27%.

After reserving judgment last fall about whether the slowdown in inflation would persist, consumers now feel assured that inflation will continue to soften.

Sentiment has resumed the upward trajectory from the all-time low measured in June of 2022, which had stalled in the late summer and fall of 2023. However, consumers expressed considerable disagreement about the future of the economy. About 41% of consumers expect good times in the year ahead for business conditions, while 48% expect bad times. This still represents a vast improvement over the past year and a half. In June of 2022, a whopping 79% of consumers expected challenging times ahead for the economy.

Sentiment is now 7% below the historical average since 1978.

Operator

Thank you for standing by. Good day everyone and welcome to the Amazon.com Fourth Quarter 2023 Financial Results Teleconference. [Operator Instructions] Today's call is being recorded.

For opening remarks, I will be turning the call over to the Vice President of Investor Relations, Mr. Dave Fildes. Thank you, sir. Please go ahead.

Dave Fildes

Hello and welcome to our Q4 2023 financial results conference call. Joining us today to answer your questions is Andy Jassy, our CEO, and Brian Olsavsky, our CFO. As you listen to today's conference call, we encourage you to have our press release in front of you, which includes our financial results, as well as metrics and commentary on the quarter. Please note, unless otherwise stated, all comparisons in this call will be against our results for the comparable period of 2022.

Our comments and responses to your questions reflect management's use as of today, February 1, 2024, only and will include forward-looking statements. Actual results may differ materially, additional information about factors that could potentially impact our financial results is included in today's press release and our filings with the SEC, including our most recent annual report on Form 10-K and subsequent filings.

During this call, we may discuss certain non-GAAP financial measures. In our press release slides accompanying this webcast and our filings with the SEC, each of which is posted on our IR website. You'll find additional disclosures regarding these non-GAAP measures including reconciliations of these measures with comparable GAAP measures. Our guidance incorporates the order trends that we've seen to date and what we believe today to be appropriate assumptions.

Our results are inherently unpredictable and may be materially affected by many factors, including fluctuations in foreign exchange rates, changes in global economic and geopolitical conditions and customer demand and spending, including the impact of recessionary fears, inflation, interest rates, regional labor market constraints, world events, the rate of growth of the internet, online commerce, cloud services, and new and emerging technologies, and the various factors detailed in our filings with the SEC.

Our guidance assumes, among other things, that we don't include any additional business acquisitions, restructurings or legal settlements, it's not possible to accurately predict demand for our goods and services, and therefore our actual results could differ materially from our guidance.

And now, I'll turn the call over to Andy.

In the first quarter of Qualcomm’s fiscal year 2024 the company delivered revenue of $9.935 billion (consensus expected $9.537 billion) and GAAP EPS of $2.46 (consensus expected $2.10). On a segment basis, QCT revenues beat estimates at $8.423 billion versus the consensus expectation of $8.051 billion. In QCT specifically, Handsets (up 16.0% Y/Y) came in better than expected at $6.687 billion versus $6.311 expected and Automotive (up +31.0% Y/Y) posted sales of $598 million versus $519 million expected. IoT sales were weaker than expected and fell -32.0% Y/Y to $1.138 billion against consensus expectations for $1.252 billion.

The company continues to make its push into the AI-at-the-edge market with its Snapdragon 8 Gen 3 Mobile Platform for smartphones. In automotive, Qualcomm is testing driving experiences enabled by Generative AI models that run locally on the Snapdragon platform. In connected devices and IoT the company has PC solutions running AI on its X Elite product, mixed reality in the XR2+ Gen 2 and an X35 5G Modem-RF system. Much of the generative AI forward devices are set to release over 2024.

Despite providing guidance that met analyst expectations, the implication behind the Handset segment in particular was concerning and caused the stock to drop 5%. Qualcomm guided to QCT revenues of $7,979, down 6.0% sequentially, suggesting that the Handset segment could be down as much as 6.50%. After last quarter’s beat and raise, it was surprising to see weakness in 2Q. Additionally, Qualcomm said it expects the Android market to be flat after leading the outperformance for the business in the first quarter. This raises market share and competition concerns as Huawei reasserts itself in China with Apple facing headwinds in the region. Qualcomm did win additional business with Samsung in the quarter and forecasts its Apple contract to endure until FY2028.

Meta demonstrated confidence in its business trajectory to investors by initiating a $0.50 quarterly dividend in the quarter in addition to a $50 billion share repurchase authorization — on top of Q4 2023 revenue and earnings and Q1 2024 revenue guidance that surpassed expectations. Advertisers have kept high levels of social investment in Facebook and Instagram as the platform offered increasing ROAS and a precision of ad metrics unavailable on any other social media platform. AI innovations have contributed to the uptick in advertising revenue as they were able to effectively solve advertisers’ challenges under new sets of privacy rules, with new models for performance metrics trained on the data points from 3.98 billion Monthly Active People. Engagement levels are also deepening on the user side given the content shifts toward third party content that AI algorithms decide users will be most engaged with.

On the updated product development roadmap for Meta, in the near term, the company is leaning into monetizing Business Messaging on WhatsApp and Messenger, including Click-to-Message Ads and Paid Messaging — which are gaining encouraging traction specifically within the U.S. Meta is seeing better-than-expected engagement and adoption of its early AI products, both on the user and advertiser side, so expanding the Advantage+ capabilities, improving Reels recommendation across the Family of Apps, and pushing out new AI assistant features will be the focus of the medium term. For the long term, the focus remains on building out the metaverse, AR, and VR, but CEO Mark Zuckerberg made a new north star clear today — developing full generalized intelligence to power the long-term platform. Meta is also focused on opening the developer side through open-sourced AI models in order to leverage 3rd party contributions to the software, given the continued “lean organization” following Meta’s year of efficiency.

In order to get to that long-term vision, Meta is stepping up CapEx investment from 20% of revenue in 2023 to ~22% of revenue in 2024, at $30-37 billion. In addition to acquiring the chips necessary to fuel data center growth, Meta is rolling out a proprietary silicon in the upcoming year along with new innovations for data center structure.

With the continued consumer strength into H1 2024, advertising guidance surpassed the consensus $33.6 billion Q1 2024 revenue estimate at a range of $34.5-37 billion. This also captures revenue inflection points in Business Messaging contribution and deepened adoption of new AI advertiser tools. Uncertainty about how the macroeconomic landscape will evolve over the coming year means H2 2024 will be subject to much tougher comps with a range of consumer/advertiser outcomes. However, continued strength in H1 2024 on a rebound from weak comps in H1 2023 drives increased confidence in Meta’s performance for the full year.

FOMC Statement

January 31, 2024

Recent indicators suggest that economic activity has been expanding at a solid pace. Job gains have moderated since early last year but remain strong, and the unemployment rate has remained low. Inflation has eased over the past year but remains elevated.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. The Committee judges that the risks to achieving its employment and inflation goals are moving into better balance. The economic outlook is uncertain, and the Committee remains highly attentive to inflation risks.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 5-1/4 to 5-1/2 percent. In considering any adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals. The Committee’s assessments will take into a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Thomas l. Barkin; Michael S. Barr; Raphael W. Bostic; Michelle W. Bowman; Lisa D. Cook; Mary C. Daly; Phillip N. Jefferson; Adriana D. Kugler; Loretta J. Mester, and Christopher J Waller.

Earnings Call Summary

Alphabet finished 2023 with another quarter of solid growth, particularly with strength in their advertising segment, devices, subscriptions services, and Cloud.

On Search, Sundar Pichai, CEO, commented that early feedback to Search Generative Experience (SGE) has been positive and they think over time Assistant will be very complementary as they develop other advanced models and Bard.

He also commented that AI is driving interest and early adoption for Cloud, and they have been able to optimize costs in various parts, which has boosted Cloud growth in the quarter.

Ruth Porat, CIO, said their guidance for elevated CapEx reflects their investment in their technical infrastructure as they see tremendous long-term opportunity with AI applications within Google across the board.

She also touched on some work streams in their effort to durably reengineer their cost base:

product prioritization and organizational design,

improving efficiency of technical infrastructures,

streamlining operations across Alphabet through use of AI,

cooperation with suppliers and vendors,

and real estate optimization.

Q2 was a record quarter, driven by the continued strength of Microsoft Cloud, which surpassed $33 billion in revenue, up 24%.

Total revenue was $62.0 billion, up 18% year-over-year, Operating income was $27.0 billion, up 33% year-over-year, representing 43.6% margin.

MSFT now has 53,000 Azure AI customers and the company has also built the world's most popular SLMs, which offer performance comparable to larger models but are small enough to run on a laptop or mobile device.

This quarter, MSFT added support for OpenAI's latest models, including GPT-4 Turbo, GPT-4 with Vision, DALL-E 3, as well as fine-tuning.

GitHub revenue accelerated to over 40% year over year, driven by all platform growth and adoption of GitHub Copilot. MSFT now has over 1.3 million paid GitHub Copilot subscribers, up 30% quarter over quarter, and more than 50,000 organizations use GitHub Copilot business.

With the acquisition, MSFT has added hundreds of millions of gamers to the ecosystem and hours streamed increased 44% year-over-year.

For Q3, MSFT expects Productivity and Business Processes revenue to grow 10% - 12% year-over-year to $19.3 - $19.6 billion, Intelligent Cloud revenue to grow 18% and 19% to $26 - $26.3 billion and More Personal Computing revenue to grow 11% - 14% to $14.7 - $15.1 billion.

COGS is expected to be between $18.6 billion to $18.8 billion, including approximately $700 million of amortization of acquired intangible assets from the Activision acquisition and operating expenses of $15.8 billion to $15.9 billion.

Executive Summary

Regeneron shares fell -1.32% in the intra-day session after the company reported third quarter earnings as domestic 2 mg EYLEA sales trailed consensus estimates. This came in spite of the in-quarter performance beating on the top and bottom line estimates (as detailed in the graphic on the next page). In addition to EYLEA HD sales beating the consensus expectation for $112 million prior to the preliminary result in early January, the franchise also gave positive signals for the long-term durability of the franchise. Several key data points suggested HD EYLEA will allow Regeneron to retain share: (1) EYLEA HD and 2 mg secured 49% of the anti-VEGF category in the quarter after reporting a decline in category share last quarter (from 46% to 45%); (2) physician enthusiasm is high and many report wanting to wait for early April, when the permanent J-code goes into effect, to ensure reimbursement before campaigning the drug to patients, and (3) EYLEA is being accepted by a broad range of patients types including those switching from 2 mg, those switching from other branded Agents & Avastin, and modest treatment-naive adoption. Dupixent and Libtayo also continue to show strong share gains, with Dupixent leading share in new-to-market products in 80% of its indications and Libtayo making headway in its approved indications. Looking forward, we are excited for additional approvals for these two drugs, but also the oncology costim platform should debut its first to market products in 2024.

The story of Peloton’s quarter is investors were disappointed by the miss on profitability estimates along with a push back in the expectation for positive FCF from Q3 2024 to Q4 2024, but on the positive end, underlying engagement trends are clearly improving with revenue surpassing estimates and guidance for Q3 subscribers surpassing expectations. In totality, signals were mixed on the near-term outlook with another expected loss in subscribers in Q4 and FY 2024 revenue guidance below expectations despite the beat in Q2. PTON shares traded down to $4.39 (-21.0%) following results given the uncertainty, especially with a lack of confidence in broader economic strength for the rest of 2024. What does not show in the stock reaction and quarterly results is what is going on behind the scenes at Peloton that is shifting the trajectory from mitigating cash burn to premium growth opportunities at the core of Peloton’s strategic advantages. Management has clearly shifted back to investing in the business at reasonable levels in order to deliver on product innovation and new horizons for Peloton software customization/offerings.

One thing messaged by CEO Barry McCarthy on the investor call was the company is now firmly on the path to arresting cash burn by Q4 2024, which enables them to invest more in future growth and product innovation. This second phase of McCarthy’s plan is expected to play out over the next 2 years, which finally offers the opportunity to return the company to growth.

The ways to get to growth messaged are through new hardware product innovation (hinting at new releases over the next 24 months), personalization in software offerings a-la-Spotify/Netflix which is McCarthy’s zone of genius, and increasing awareness of products in key geographies which remain low (unaided brand awareness: 55% in the U.S., 20% in Germany, and <20% in Latin America). The management team seems to be leaning back into premium/customized offerings as a north star for growth, which is a relief reflecting on the past two years of Peloton’s lower-priced and more accessible offerings which really haven’t inflected growth in financials.

Thursday

February 2, 2024

12 PM

Hello everybody!

Happy Thursday! Today is the first day of February, which is Black History Month. For today's meeting, we have asked each of the investment team members to prepare a 1 or 2 minute discussion on a prominent figure. Everyone is encouraged to present!

Agenda:

I. Blue Room LLC Updates

II. Blue Room Investing

III. Blue Room Housing

IV. Blue Room Ag

V. Blue Room Art

_____

Icebreaker: Black History Month

According to Wikipedia, this month of celebration of Black history and culture has been observed in forms dating back to 1926, with mainstream American adoption in the late 60s (Kent State University) and in 1976 by President Gerald Ford during the bicentennial year of our country. Today at Blue Room, we are celebrating by asking team members to present prominent people during our company meeting.

Beginning with lunch at Osaka Ramon

BLUE ROOM ART FIELD TRIP

Thank you VISIONS WEST GALLERY_ not only for being one of our FAVORITES, but for the personal tour of the current breathtaking show CONTEMPORARY COWBOY.

10% OF ALL BLUE ROOM REVENUES GO DIRECTLY TO FUND OUR NON PROFIT TOGETHERISM.

WE CAN ACCOMPLISH ANYTHING TOGETHER.

These materials do not purport to be all-inclusive or to contain all the information that a prospective investor may desire in considering an investment. These materials are intended merely for preliminary discussion only and may not be relied upon for making any investment decision. Any discussion or information contained in this presentation does not serve as a receipt of, or as a substitute for, personalized investment advice from Blueroom or your advisor.

This publication does not constitute an offer to sell or a solicitation to buy any securities in any fund, market sector, strategy or any other product. Investing is speculative and involves substantial risks (including, the risk of loss of the investor’s entire investment). Past performance is not indicative of future results, and there can be no assurance that the future performance of any specific investment, investment strategy, or product will be profitable.

For more information about us and our general disclosures contact us directly.