Weekend Update #155

Thank you for your continued support and engagement. Each week, we're sharing what companies we're researching and the what, the who and the how that we think makes the companies interesting and unique. This roundup is brought to you weekly by a group of interns, creative minds, artists and investors who believe that through best in class investing along with the democratization of financial education we can do great things together. Enjoy, Explore and Share.

The trading week following Thanksgiving and ending on the first day of December 2023 comprised several key earnings releases and economic data releases.

On Tuesday after market close, Cybersecurity-provider CrowdStrike Holdings (CRWD) reported revenue of $786 million, exceeding estimates of $777.4 million and issued 2024 revenue guidance of $3.05 billion, exceeding estimates of $3.04 billion, causing the stock to rise as high as 5.7% on Wednesday. Meanwhile enterprise cloud-based HR services provider Workday (WDAY) climbed as much as 9.5% after reporting adjusted EPS of $1.53, beating the Street’s $1.40 figure, and revenue of $1.87 billion versus the Street’s $1.85 billion. Further, the company raised subscription revenue guidance from the previous $6.57–$6.59 billion range to $6.60 billion.

On Wednesday, customer relationship management software provider Salesforce (CRM) rose by as much as 9.6% after also reporting adjusted EPS and revenue that beat Street estimates. Third quarter revenue came in at $8.72 billion versus consensus’ $8.71 billion, while adjusted EPS of $2.11 exceeded estimates of $2.06. For 2024 the company narrow its revenue guidance range from $34.7–$34.8 billion to $34.75–$34.8 billion, in line with the Street’s $34.79 billion estimate, and it raised its adjusted EPS range from $8.04–$8.06 to $8.18–$8.19, exceeding the Street’s $8.06 figure. Additionally, the company raised its adjusted operating margin guidance from 30% to 30.5%. Other companies that reported this week include Ambarella and Synopsis, the former showing signs of stabilization and positive inventory trends while the latter electronic design automation software provider beat expectations and signaled it is exploring strategic alternatives for its Software Integrity business.

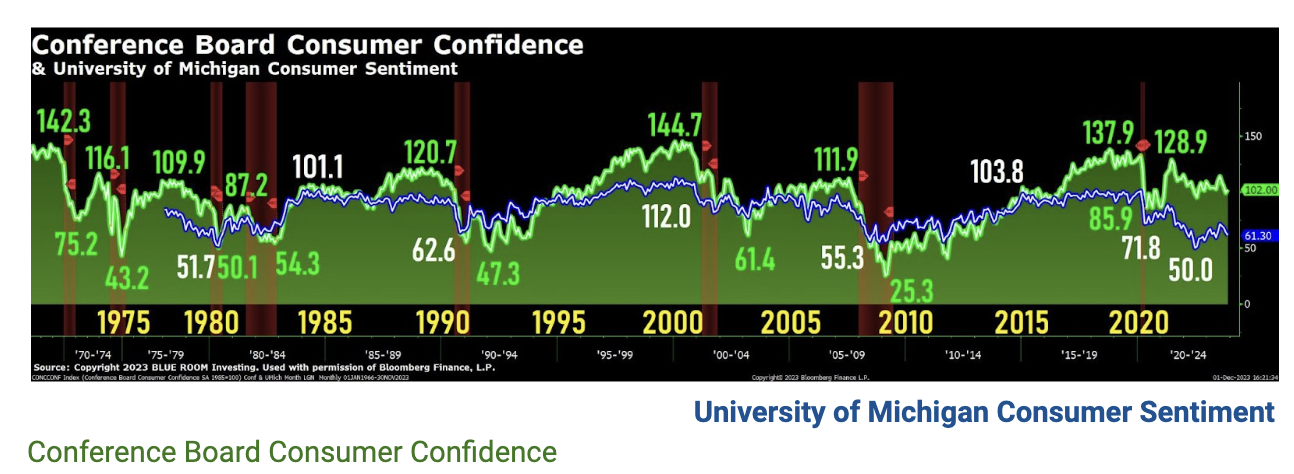

On the economic front, we saw a downside surprise on new home sales, whose annualized figure of 679K came in below the anticipated 721K figure. Despite this, the FHFA House Price Index showed a 0.6% month-over-month increase, exceeding the expected +0.5%. Conference Board Consumer Confidence reported a 102 figure, above the 101 expected. Q3 GDP came in hot at 5.2%, while personal consumption of 3.6% came in below the expected 4.0% increase. Perhaps one of the most key series of readings this week was PCE, with quarter-over-quarter core PCE of 2.3%, “headline” PCE of 3.0% and core PCE of 3.5% all came in line or below expectations—all welcome news for the Fed, and markets, which helped propel the S&P and Dow Jones 1.03% and 2.77% this week on bets that the Fed was likely done hiking rates thanks to an increasingly possible soft landing thanks to economic data showing a resilient economy despite easing price pressures.

The week was capped off by Fed Chair Powell’s appearance at Spelman College in Atlanta, Georgia, in which he said current monetary policy is “well into restrictive territory” while reiterating speculation on when might policy might ease is “premature”, which runs counter against recent market bets that the Fed will begin cutting rates as soon as March.

Weekly Performance

S&P 500 4,594.63 +1.03%

Dow Jones 36,245.50 +2.77%

Nasdaq 14,305.03 +0.26%

Key Economic Readings Next Week

Monday, December 4 — Factory Orders, Durable Goods Orders

Tuesday, December 5 — S&P Global US Composite & Services PMI; ISM Services Index

Wednesday, December 6 — ADP Employment Change, Trade Balance

Thursday, December 7 — Challenger Job Cuts; Wholesale Inventories and Trade Sales

Friday, December 8 — Change in Nonfarm Payrolls; Unemployment Rate; UMich Sentiment

There is no better insight gleaned into the strength of the American consumer than by looking into the biggest shopping days of the year — Black Friday and Cyber Monday — which proved to be filled with clues into the resiliency of consumer spending through 2023.

Data collected by Adobe Analytics showed that consumers spent $9.8 billion on Black Friday, up 7.5% year-over-year, and spent $12.4 billion on Cyber Monday, up 9.6% year-over-year. Both figures surpassed expectations for the level of spending, given some prior signs of caution by consumers, and the data points further highlight the resiliency of the American consumer seen throughout 2023.

A few key themes have emerged from this year:

Deal-driven, price-sensitive shoppers

The YOLO consumer

Buy-now-pay-later’s surge in funding holiday shopping

Shopify data from Black Friday/Cyber Monday sales above shows the consistent growth in e-commerce and continued strength in its merchants’ sales through this holiday season. Part of the expansion can be attributed to Shopify’s success in attracting new merchants to its e-commerce platform, however, sales during Black Friday and Cyber Monday did not show any signs of deceleration compared to prior year periods — despite some warning signs on consumer strength appearing elsewhere in the quarter.

Credit card data from Bloomberg showed that “In the three months ahead of the all-important holiday shopping season, a group of retailers that cater to the upper middle class — including Apple, Coach, and Nordstrom — saw its biggest sales drop in two years.” The upper middle class is an important socioeconomic segment to analyze as the group tends to cut back on spending quicker than other groups, and the warning signals from those earnings $100,000 or more annually starting to cut back on spending have started to flash since September.

Colette Kress — Chief Financial Officer, Nvidia Corporation

Q3 was another record quarter. Revenue of $18.1 billion was up 34% sequentially, and up more than 200% year-on-year, and well above our outlook of $16 billion.

Starting with Data Center. The continued ramp of the NVIDIA HGX platform based on our Hopper Tensor Core GPU architecture, along with InfiniBand end-to-end networking, drove record revenue of $14.5 billion, up 41% sequentially, and up 279% year-on-year. NVIDIA HGX with InfiniBand together are essentially the reference architecture for AI supercomputers and Data Center infrastructures.

Some of the most exciting generative AI applications are built and run on NVIDIA, including Adobe Firefly, ChatGPT, Microsoft 365 Copilot, CoAssist -- Now Assist with ServiceNow, and Zoom AI Companion. Our Data Center compute revenue quadrupled from last year, and networking revenue nearly tripled. Investments in infrastructure for training and inferencing large language models, deep learning, recommender systems, and generative AI applications is fueling strong broad-based demand for NVIDIA-accelerated computing. Inferencing is now a major workload for NVIDIA AI computing.

Consumer Internet companies and enterprises drove exceptional sequential growth in Q3, comprising approximately half of our Data Center revenue, and outpacing total growth. Companies like Meta are in full production with deep learning, recommender systems, and also investing in generative AI to help advertisers optimize images and text. Most major consumer Internet companies are racing to ramp-up generative AI deployment. The enterprise wave of AI adoption is now beginning. Enterprise software companies such as Adobe, Databricks, Snowflake, and ServiceNow are adding AI co-pilots and assistants to their platforms. And broader enterprises are developing custom AI for vertical industry applications, such as Tesla in autonomous driving.

Cloud service providers drove roughly the other half of our Data Center revenue in the quarter. Demand was strong from all hyperscale CSPs, as well as from a broadening set of GPU-specialized CSPs globally, that are rapidly growing to address the new market opportunities in AI.

Key Metrics and Business Highlights

Customers with annual contract value (ACV) equal to or greater than $250,000 were 453, up from 420 as of October 31, 2022. Seven of the deals that closed in the quarter ended October 31, 2023 had ACV equal to or greater than $500,000, two of which had ACV greater than $1.0 million.

Dollar-based retention rate (DBRR) was 108%, compared to 109% as of October 31, 2022.

Annual Recurring Revenue (ARR) was $396.0 million compared to $350.7 million as of October 31, 2022, representing ARR growth of 13%.

Hosted an international series of Subscribed Connect events in London, Paris, Munich, Stockholm and Tokyo, announcing multiple product enhancements including:

A new native Mediation Engine within Zuora for Consumption, which helps companies create flexible meters and consolidate usage data, unlocking new customer insights to rapidly experiment with pricing and better align with customer value.

Subscriber IQ, a new Zephr capability, which helps product and growth teams glean valuable subscriber insights through a connected view of subscribers combined with industry benchmarks.

Zuora Integration Hub, one place for drag-and-drop integration that makes it even faster for technical teams to configure and maintain Zuora’s 60+ pre-built connectors to CRM, CPQ, ERP, payment gateways and more.

Zuora Extension Studio, which empowers admins to extend Zuora for changing business requirements, configure unique use cases and change monetization processes quickly.

Announced a partnership with Sovos to help global businesses meet e-invoicing mandates.

Zuora expanded its services with Google Fiber, Alphabet’s high-speed broadband internet service that spans 15 states and counting. Now, Zuora will power GFiber’s full order-to-revenue process as they continue to grow.

New customers and go-lives included LinkedIn, FreshBooks and Dark Matter Technologies.

Jamey Mock – Chief Financial Officer

Yes. Thanks. And again thanks for having us. Yes. So I mean you kind of said it in some of your opening remarks there that we think we're in a great position. Yes. We've rode a wave here, but in – 2024 might be a low point for us.

But we wanted to set out kind of our philosophy here, which is we have a tremendous pipeline, a tremendous platform, and we want to invest in it because we think it's a true organic growth driver. So we've come out and said, hey, we're going to invest in these products and in R&D over the next couple of years and use a fair amount of our capital and try to launch 15 new products by 2028, which is outstanding. It would be somewhat unprecedented. So that was the philosophy in terms of laying out the framework to say let's make sure we understand the baseline for 2024, and we said that sales will be about $4 billion, and that we'd use about $1 billion of cash in 2024, and we're starting at $13 billion. Then again it would probably happen we'd return to growth in 2025 as we launch more products, but again use $2 billion to $3 billion of capital.

Then by 2026, we think that the portfolio and what we have at that point, we will break even. We are cash conscious, and we always all have been. Then I think we wanted to show that, hey, volume might have changed, this wave might be a little bit behind us, but Covid is here to stay. We will launch new products. We are going to invest in this platform, and that was kind of what we came out with to make sure our investors understood that.

November 21, 2023

Comparable Sales Declined 6.9%

GAAP Diluted EPS of $1.21

Non-GAAP Diluted EPS of $1.29

MINNEAPOLIS--(BUSINESS WIRE)-- Best Buy Co., Inc. (NYSE: BBY) today announced results for the 13-week third quarter ended October 28, 2023 (“Q3 FY24”), as compared to the 13-week third quarter ended October 29, 2022 (“Q3 FY23”).

“Today we are reporting better-than-expected profitability on slightly softer-than-expected revenue for the third quarter,” said Corie Barry, Best Buy CEO. “These results demonstrate our ongoing, strong operational execution as we navigate through the near-term sales pressure our industry has been experiencing for the past several quarters.”

Barry continued, “In the more recent macro environment, consumer demand has been even more uneven and difficult to predict. Based on the sales trends in Q3 and so far in November, we believe it is prudent to lower our annual revenue outlook. The midpoint of our annual non-GAAP diluted EPS guidance is slightly higher than the midpoint of our original guidance as we entered the year.”

“We are excited for the important holiday season and are prepared for a customer who is very deal-focused with promotions and deals for all budgets, new shopping experiences, an expanded product assortment, and fast and free fulfillment,” continued Barry. “I want to thank our associates for their resilience, determination, and relentless focus on our customers. I continue to be very proud of the way our teams are managing the business today and preparing for our future.”

Erick Lucera – Chief Financial Officer

Well, obviously, from a 30,000 foot view, we're really excited about the progress that Vertex is making, not only for the patients, but also for the field of gene editing. But as you mentioned, there are a few differences between our approach and their approach. The first is they're using Cas9 and we're using Cas12a, so it's a different enzyme. And we're targeting the gamma globin promoter, which we believe, based on our research, leads to a little bit better hemoglobin data. So we think that'll be a point of differentiation that we'll see play out over time, and we're seeing it already, so...

Liisa Bayko – Analyst

Great. And are you – how – you have intellectual property rights to Cas9. Is that correct?

Erick Lucera – Chief Financial Officer

Yes.

Liisa Bayko – Analyst

And what are you thinking about, I guess, your kind of approach when Exa-cel does get approved? Curious how you think about it.

Erick Lucera – Chief Financial Officer

Yes, right. We can't comment on any specific program or product or company in terms of discussions, but we can talk broadly. We think that we have foundational patents for both Cas9 and Cas12. We've got great intellectual property estate licensed from Harvard, MIT, and the Broad. And we are open to anyone that wants to talk to us about getting a license. I'll leave it at that.

Speaker: Helmy Eltoukhy — Co-Chief Executive Officer

Yes, it's great to be here presenting the Guardant story.

So we started Guardant about 11, 12 years ago now really, with this idea of giving patients more time — More time free from cancer, more time with their loved ones, with their families, and friends

We developed a technology that really pioneered the liquid biopsy space in terms of the ability to take a tube of blood and really extract as much information from it as we can. It really centered on essentially cell free DNA or DNA that's being shed from dying cells in the body and mostly cancer cells in the body.

And we developed a new chemistry that allowed us to extract that DNA with extremely high efficiency, employed next generation sequencing techniques, and really used a powerful new informatics platform to be able to learn how to extract those signals with very high fidelity in high sensitivity, and use the fact that we were acquiring a lot of data to aggregate that data and make the algorithms better over time. Then this is really the sort of core of what we do at Guardant.

This allowed us to unlock three major verticals in cancer, really the idea of therapy selection, where we started with, we launched the first test in 2014. That's a $10 billion total addressable market in the U.S., with close to a million advanced cancer patients, over 700,000 advanced cancer patients. And now that test, the 360 franchise, Guardant360 franchise is the leading liquid biopsy in the United States and soon to be globally.

The second vertical is minimum residual disease, to $20 billion opportunity. There are over 15 million cancer survivors in the United States. So these are individuals that had early-stage cancer, and were cured through either resections or sort of associated adjuvant therapy. The idea is to monitor those patients with a blood test for reccurrence of disease.

And the largest market opportunity is screening, which is $100 billion U.S. market opportunity. There are over 120 million individuals who are average risk in the United States that should get annual or semi-annual testing in terms of early detection of cancer. We just finished a very large trial. We think we'll have the first FDA-approved Medicare-reimbursed liquid biopsy for screening sometime next year.

AMBARELLA INC., THIRD QUARTER FINANCIAL RESULTS

SANTA CLARA, Calif., Nov. 30, 2023 (GLOBE NEWSWIRE) -- Ambarella, Inc. (NASDAQ: AMBA), an edge AI semiconductor company, today announced financial results for its third quarter of fiscal year 2024 ended October 31, 2023.

Revenue for the third quarter of fiscal 2024 was $50.6 million, down 39% from $83.1 million in the same period in fiscal 2023. For the nine months ended October 31, 2023, revenue was $174.9 million, down 31% from $254.3 million for the nine months ended October 31, 2022.

Gross margin under U.S. generally accepted accounting principles (GAAP) for the third quarter of fiscal 2024 was 59.3%, compared with 62.2% for the same period in fiscal 2023. For the nine months ended October 31, 2023, GAAP gross margin was 60.6%, compared with 62.6% for the nine months ended October 31, 2022.

GAAP net loss for the third quarter of fiscal 2024 was $41.7 million, or loss per diluted ordinary share of $1.04, compared with GAAP net loss of $19.8 million, or loss per diluted ordinary share of $0.51, for the same period in fiscal 2023. GAAP net loss for the nine months ended October 31, 2023 was $108.8 million, or loss per diluted ordinary share of $2.74. This compares with GAAP net loss of $54.3 million, or loss per diluted ordinary share of $1.42, for the nine months ended October 31, 2022.

Financial results on a non-GAAP basis for the second quarter of fiscal 2024 are as follows:

Gross margin on a non-GAAP basis for the third quarter of fiscal 2024 was 62.6%, compared with 63.5% for the same period in fiscal 2023. For the nine months ended October 31, 2023, non-GAAP gross margin was 63.5%, compared with 64.0% for the nine months ended October 31, 2022.

Non-GAAP net loss for the third quarter of fiscal 2024 was $11.2 million, or loss per diluted ordinary share of $0.28. This compares with non-GAAP net income of $9.5 million, or earnings per diluted ordinary share of $0.24, for the same period in fiscal 2023. Non-GAAP net loss for the nine months ended October 31, 2023 was $23.2 million, or loss per diluted ordinary share of $0.59. This compares with non-GAAP net income of $34.1 million, or earnings per diluted ordinary share of $0.88, for the nine months ended October 31, 2022.

ZM Q3 FY2024 Earnings Call Content Summary

Zoom reported better-than-expected Q3 FY '24 results with revenue coming to $1,137 million (+3.2% y/y), about $17 million higher than the high-end guidance. For Q4, revenue is targeted to grow at around 1.0%, resulting in full year revenue growth of 2.6%.

In terms of product, Zoom Phone reached ~7 million paid seats, Zoom Contact Center reached ~700 customers as of quarter-end, and the number of Zoom One customers including Zoom Phone grew ~330% y/y.

Deferred revenue was $1.32 billion, down ~3% from Q3 of last year. For Q4, deferred revenue is expected to be down 6% to 8% y/y, partially driven by shorter billing frequencies on Enterprise deals arising from the high interest rate environment.

Given the strength and profitability in collections, Zoom increases the free cash flow outlook for FY '24 in the range of $1.34 billion to $1.35 billion, which at the midpoint would represent 13% y/y growth.

The number of Enterprise customers grew 5% y/y to approximately 219,700. The trailing 12-month net dollar expansion rate for Enterprise customers in Q3 came in at 105%. Zoom ended the quarter with 3,731 customers contributing more than $100,000 in trailing 12 months revenue.

In Q3, Zoom showcased newly-released innovations like Zoom AI Companion, Zoom AI Expert Assist and Quality Management for the Contact Center. Zoom AI Companion is especially noteworthy for being included at no additional cost to the paid plans.

Heather Stark – Chief Financial Officer

Yes, absolutely. It's been an eventful couple of years, I would say and a really good and interesting start to our turnaround. If you think of who Weight Watchers is and the fact that we have been in existence for 60 years as a peer-to-peer accountability led behavior change, weight loss program, a lot has changed in those 60 years, but really dramatically in the last two.

If we think about sort of pre-Covid, our consumers were really shifting to start to engage with us digitally. We had started as a workshop business and in real life, peer-to-peer accountability experience and really accelerated by Covid, we saw a dramatic shift to consumers wanting to engage with us digitally and that presented an opportunity to us to lean into and really think about becoming a digital-first company.

Our app was in existence pre-Covid but it was really as a second screen as a companion to the weight loss experience that people were experiencing with us in real life. We really leaned into becoming a digital-first company where this is the first screen experience – taking from what we know to be the gold standard in our weight management business of coaching accountability and community and figuring out ways to bring that to consumers digitally. Then 1.5 years ago, we were joined by our new CEO, Sima Sistani, and that has really propelled us forward under her leadership.

She is a digital product leader, a community builder in her background. When I think of the amazing accomplishments we've had so far in those 18 months, it's been an exciting time for us. So Sima joined us and really quickly identified the need to simplify how we show up to simplify our product. That was a really big initiative and it's still underway. So looking at our app, our product and saying, what are consumers engaging in and let's deliver those things that consumers engage in most.

So streamlining and simplifying the app experience was really important and sort of cleansing those things that consumers weren't engaging in and serving up a simpler version of the app on which to build a forward and engaging experience. She also undertook an immense reorganization of our company, and we looked at every way we were operating.

This is a business that she joined that was in successive years of decline and she looked at ways to help us rethink our cost base. So we relooked our workshop footprint. We underwent a significant retail, real estate restructuring this past year and also end-to-end our team structure. So in operating expenses, those teams that are focused on our workshop business, we really had to rightsize how we were thinking about showing it up in that space to make sure we were having good throughput in margins in that business. And also in our G&A, so the cost structure of our teams globally, we really leaned into simplifying those globally. You see that to your question, how are we seeing all of this read through?

Consumer sentiment fell a modest 2.5 index points, or 4%, from October to 61.0 in November.

While this marks the fourth consecutive month of declines, November’s reading reflects a balance of factors, some of which improved while others worsened. More favorable current assessments and expectations of personal finances were offset by a notable deterioration in expected business conditions. In particular, long-run business conditions plunged by 15% to its lowest since July 2022.

Younger and middle-aged consumers exhibited strong declines in economic attitudes this month, while sentiment of those age 55 and older improved from October.

Year-ahead inflation expectations rose to 4.5% this month, up from 4.2% in October — reaching its highest reading since April 2023. Long-run inflation expectations rose from 3.0% last month to 3.2% this month, a reading last seen in 2011. These expectations have risen in spite of the fact that consumers have taken note of the continued slowdown in inflation; the share of consumers blaming high prices for eroding their living standards fell from 47% in October to 40% this month. At this time, consumers appear worried that the softening of inflation could reverse in the months and years ahead. Likewise, despite easing prices at the pump, one-year gas price expectations rose to its highest reading since June 2022, and five-year gas price expectations are their highest since March 2022.

The financial demand for crude oil continued to atrophy throughout November as continued economic uncertainty questioned the strength of demand while better-than-anticipated non-OPEC supply provided further downward price pressure. As fears of escalation in the Middle East continued to fade and concerns surrounding the multi-million barrel per day deficit in the fourth quarter have all but abated, the market driving events of the past month focused largely on OPEC and IEA data releases, as well as the OPEC+ production meeting.

The West Texas Intermediate benchmark began the month bobbing around $80/bbl – a near 13% decline from the highs reached following fears of Iranian escalation in the Middle East. While the Brent benchmark traded near $85/bbl – a price that many oil analysts consider palatable to the Saudis, though not ideal – the price stood in profound defiance to the notion that the fourth quarter of 2023 was scheduled to be one of notable declines in global crude inventory levels. Indeed, at this time, crude oil inventories were beginning to show seasonal strengthening. To this end, on November 5, the Saudi Press Agency announced that “the Kingdom of Saudi Arabia will continue the voluntary cut of one million barrels per day, which went into implementation in July 2023 and was later extended until the end of December 2023. Thus, the Kingdom’s production in the month of December 2023 will be approximately 9 million barrels per day…The source confirmed that this additional voluntary cut comes to reinforce the precautionary efforts made by OPEC Plus countries with the aim of supporting the stability and balance of oil markets.”

Hello Blue Room,

Welcome to our 134th Global Meeting. We have a lot on deck with year end reviews and planning across each of our businesses.

Agenda:

I. Blue Room Investing

II. Blue Room Impact

__ Agriculture

__ Housing

__ Art

Icebreaker:

Today is the last day of November, the month said to be one of comings and goings. This week, we note the passing of Berkshire Hathaway Vice Chair Charlie Munger, Secretary of State Henry Kissinger and First Lady Rosalyn Carter. Who are the seniors in your life that have had an impact on you, and what do you admire about them?

____________________

BLUE ROOM

Global Meeting Archive:

BLUE ROOM (TM)

Subscribe to our weekly newsletter:

blueroominvesting.com/weekend-update

WDAY Q3 FY2024 Earnings Call Content Summary

WDAY reported a better-than-expected Q3 result with Subscription revenue of $1.69 billion, up 18% y/y, Professional services revenue of $175 million, leading to total revenue of $1.87 billion, growth of 17%. The 24-month subscription revenue backlog was $10.58 billion at the end of Q3, up 23%.

Non-GAAP operating income was $462 million, resulting in a non-GAAP operating margin of 24.8%. Margin strength relative to our guidance was driven by revenue outperformance and the timing of certain expenses and investments. Q3 operating cash flow was $451 million, growing 10%.

Following the momentum in Q3, WDAY raised their full year FY '24 subscription revenue guidance to $6.598 billion, representing 19% y/y growth. Professional services revenue is expected to be $158 million in Q4 and $652 million for the full year.

FY '24 non-GAAP operating margin guidance is raised to 23.8%, and for Q4, non-GAAP operating margin of approximately 23.5%. The FY '24 non-GAAP tax-rate remains at 19%. FY '24 operating cash flow is expected to be $1.975 billion, growth of 19%, and FY '24 capital expenditures of approximately $250 million.

WDAY announced new full platform customers for Workday Financial Management and Workday Human Capital Management. In Q3, WDAY surpassed 5,000 core Workday Human Capital Management.

WDAY announced several AI updates, including multiple generative AI capabilities; new AI capabilities in Workday Adaptive Planning; a Manager Insights Hub that surfaces automated insights for managers to develop their teams; and enhancements to Workday Extend to enable developers to leverage Workday AI services.

WDAY expanded partnership with ADP to help deliver an enhanced frictionless global payroll, compliance, and HR experience for joint customers, and expanded partnership with Accenture to help companies accelerate their adoption of skills-based talent strategies.

LET IT SNOW

LET IT SNOW

LET IT SNOW.

WHERE IT GROWS.

DON’T BE NAUGHTY.

BE NICE.

BUY LOCAL.

COLORADO CRAFTED

++ SHIPS NATIONWIDE ++

DRYLAND DISTILLERS

++ AVAILABLE FOR PICK UP IN LONGMONT, COLORADO ++

10% OF ALL BLUE ROOM REVENUES GO DIRECTLY TO FUND OUR NON PROFIT TOGETHERISM.

WE CAN ACCOMPLISH ANYTHING TOGETHER.

These materials do not purport to be all-inclusive or to contain all the information that a prospective investor may desire in considering an investment. These materials are intended merely for preliminary discussion only and may not be relied upon for making any investment decision. Any discussion or information contained in this presentation does not serve as a receipt of, or as a substitute for, personalized investment advice from Blueroom or your advisor.

This publication does not constitute an offer to sell or a solicitation to buy any securities in any fund, market sector, strategy or any other product. Investing is speculative and involves substantial risks (including, the risk of loss of the investor’s entire investment). Past performance is not indicative of future results, and there can be no assurance that the future performance of any specific investment, investment strategy, or product will be profitable.

For more information about us and our general disclosures contact us directly.