Weekend Update #140

Welcome to Blue Room's Weekend Update. Each week, we're sharing what companies we're researching and the what, the who and the how that we think makes the companies interesting and unique. This roundup is brought to you weekly by a group of interns, creative minds, artists and investors who believe that through best in class investing along with the democratization of financial education we can do great things together. Enjoy, Explore and Share.

Stocks declined as the S&P500 and Nasdaq fell for their third week in a row while the Dow Industrial Average fell 2.2%, its biggest weekly loss since March, as worries about China and higher global interest rates cause investors to take caution.

Fed minutes revealed officials remain concerned that inflation would fail to recede and suggested further tightening may be required. Fed Chair Powell is set to speak at Jackson Hole next week which could provide more insight into the direction the central bank is leaning with respect to additional rate hikes.

Last week, China’s economy showed signs of slowing as exports fell 14.5% in July, the biggest decline since February 2020. Retail data also showed consumer spending has been slowing, hindering the government’s efforts for an economic rebound coming out of pandemic lockdowns.

This week, China has seen worsening conditions as large firms show varying levels of distress.

Country Garden Holdings Co., one of the largest property developers in China, saw sales plunge and is nearing default after it failed to meet an initial deadline to pay coupons on dollar bonds. China Evergrande Group, the real estate firm whose default in 2021 accelerated a nationwide property debt crisis, sought Chapter 15 bankruptcy protection in New York on Thursday. Additionally, Zhongzhi Enterprise Group Co., a Chinese “shadow bank” which manages more than 1 trillion yuan ($137 billion) of assets, hired KPMG to review its balance sheet amid a worsening liquidity crunch. As a result of these impending crises, Chinese authorities are reportedly asking investment funds to avoid being net sellers of equities, as a rout in the nation’s financial markets deepened.

Crypto also saw weakness this week with Bitcoin leading the decline, briefly falling roughly 12% to $25,234 on Thursday, its lowest level since June. The plunge was caused by $1 billion worth of liquidations over the 24 hour period, the largest liquidation since FTX collapse in November, sending it into a downtrend.

Weekly Performance

S&P 500 4,369.71 -2.11%

Dow Jones 34,500.66 -2.21%

Nasdaq 13,290.78 -2.59%

Key Economic Readouts This Week

Retail Sales Advance M/M — Actual: 0.7% Estimate: 0.4%; Prior: 0.3%

Empire Manufacturing — Actual: -19.0; Estimate: -1.0; Prior: 1.1

Housing Starts M/M — Actual: 3.9%; Estimate: 1.1%; Prior: -11.7%

ADP Employment Change — Actual: 324k; Estimate: 190k; Prior: 497k

Initial Jobless Claims — Actual: 239k; Estimate: 240k; Prior: 250k

Continuing Claims — Actual: 1,700k; Estimate: 1,716k; Prior: 1,684k

Thank you Blue Room Analyst NICK PEART.

Company Profile

CAVA Group owns and operates Mediterranean fast-casual restaurants. The Company offers desserts, beverages, and other fast food products, as well as producing dips, spreads, and dressings. CAVA Group serves customers in the United States.

__

Brett Schulman — Co-Founder and Chief Executive Officer

Thanks, Matt. Let me start by welcoming everyone to CAVA's first quarterly call as a publicly-held company. We're pleased with how the market has received CAVA, but, as you'll hear, our focus is on the long-term—that's running a great business and building a durable brand that consistently delivers results.

Becoming a public company, while a milestone event, was not the destination, but the beginning, of the next chapter of our journey. CAVA is creating and defining the next cultural cuisine category, and our results in the second quarter of 2023 demonstrate the broad appeal of our innovative, authentic Mediterranean concept and the significant white space opportunity in front of us.

We're successfully opening restaurants in new and established markets. We continue to deliver powerful unit economics, and we've already made significant investments in building an efficient, scalable organization, putting the company in a strong position to deliver on our extraordinary potential for growth. We are proving that bringing heart, health, and humanity to food is a powerful formula for success.

In the second quarter of 2023, we delivered CAVA revenue growth of 62%; 18.2% CAVA same restaurant sales growth, including 10.3% traffic growth; 16 net new restaurants, ending the quarter with 279 restaurants, a 43.1% increase year-over-year; adjusted EBITDA of $21.6 million, a $15.7 million increase over the second quarter of 2022; and net income of $6.5 million.

Our Q2 results and ability to capitalize on the opportunities ahead are grounded in our three strategic pillars. First, we are solidifying our category-defining Mediterranean brand. Our broad appeal and proven portability support strong restaurant openings in new and existing markets. We opened 16 net new CAVA restaurants during the second quarter, including two new states, Missouri and Rhode Island, along with continued expansion in Massachusetts, Texas, Georgia, and Colorado. We now expect 65 to 70 net new CAVA restaurant openings this year, and have built our 2024 and 2025 pipeline to support annual unit count growth of at least 15%.

Executive Summary

TGT shares traded higher by nearly 7.0% in pre-market, and now +4.5% during the trading day. Despite missing their own topline guidance (the company forecasted a low single-digit comp sales decline for the quarter, but fell mid-single digits), profit margins increased ahead of expectations due to better inventory management. The company also lowered the full year revenue and EPS guidance as detailed in the infographic, but the stock trades higher likely due to the implications behind positive revenue comps and normalized margins expected for next year.

Operating Results

Comparable sales declined 5.4 percent in the second quarter, reflecting comparable store sales declines of 4.3 percent and comparable digital sales declines of 10.5 percent. Total revenue of $24.8 billion was 4.9 percent lower than last year, reflecting a total sales decline of 4.9 percent partially offset by a 1.3 percent increase in other revenue. Second quarter operating income of $1.2 billion was 273.0 percent higher than last year, driven by a higher gross margin rate.

Second quarter operating income margin rate was 4.8 percent in 2023, compared with 1.2 percent in 2022. Second quarter gross margin rate was 27.0 percent, compared with 21.5 percent in 2022, reflecting lower markdowns and other inventory-related costs, lower freight costs, retail price increases, and lower supply chain and digital fulfillment costs. These benefits were partially offset by higher inventory shrink. Second quarter SG&A expense rate was 20.9 percent in 2023, compared with 19.2 percent in 2022, reflecting the de-leveraging impact of lower sales combined with higher costs, including continued investments in pay and benefits and inflationary pressures throughout our business, partially offset by disciplined cost management.

Executive Summary

MNDY shares are poised for upward pressure in the second half of the year as product adoption accelerates revenue and margin expansion. Top-of-funnel pipeline remains healthy, while churn and downgrades have remained stable, positioning MNDY favorably as IT budgets look to rebound from earlier in the year. Through monday Sales CRM, monday Dev, and AI assistant, monday.com has multiple go-to-market strategies for new client acquisition as well as pursue cross-sells and upsells within its existing client base.

—

Roy Mann — Co-Founder & Co-Chief Executive Officer

Thank you, Byron, and thank you, everyone, for joining us today. In the second quarter, we continued to make significant strides in executing our long-term strategy, delivering exceptional results. Revenue grew 42% as demand for our customers remained healthy. We continued to demonstrate improved operating efficiency and cash generation, reflecting our ongoing commitment to driving sustainable growth. Eliran will talk you through our financial performance in more detail. This quarter, we are thrilled to announce the completion and release of mondayDB 1.0 to all our accounts. This is the initial version of our brand-new infrastructure for the Work OS platform. With mondayDB, customers are already experiencing large and more complex boards loading five times faster, enabling them to work more efficiently and handle data-intensive and complicated workflows.

Future releases of mondayDB will provide even more speed enhancements, scalability and functionality. In Q2, we also launched our AI Assistant and introduced several new AI capabilities. These include automated task generation, formula builder, email composition and content generation. Additionally, we opened our AI Assistant infrastructure to external developers and hosted a global AI Hackathon, which generated tremendous interest. With over 1,600 registrants and more than 40 AI apps developed, the hackathon showcased the enthusiasm and talent within our monday.com community. We have also been working to optimize our infrastructure and interface to enhance the user experience and reinforce a robust multi-product ecosystem. We see an extraordinary opportunity to enhance cross-selling efforts, strengthen inter-department organizational connection and solidify monday.com as a vital partner across all business use cases.

Company Profile

Sweetgreen manages a chain of salad restaurants. The company offers salads, frozen yogurts, nutritional specialities, and seasonal selections. It also provides stainless steel bottles, gift cards, shirts, salad blaster bowls and reusable shopping bags through its online stores.

__

Jonathan Neman — Co-Founder and Chief Executive Officer

Good afternoon, everyone. I've shared before that I believe times like these create opportunities for companies with great brands, large addressable markets and loyal customers. Great businesses have to be and companies, balancing growth and profitability.

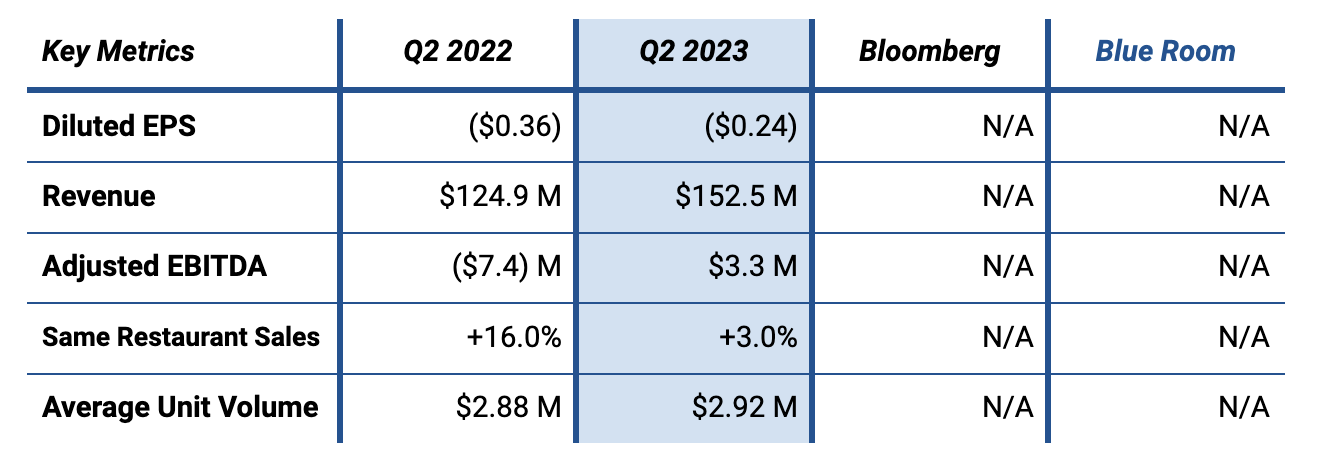

In the second quarter, we put our words into action generating 22% year-over-year revenue growth, delivering a restaurant level profit margin of 20.4% and adjusted EBITDA of $3.3 million—our first quarter of positive adjusted EBITDA as a public company. This milestone demonstrates our commitment to disciplined capital efficient growth. I want to extend my gratitude to every Sweetgreen team member for their hard work and dedication in delivering these results.

We reported second quarter revenue of $152.5 million, representing 22% year-over-year growth and Same-Store Sales growth of 3%. Our Same-Store Sales growth was driven by an increase in price and traffic, with a partial offset from mix. Total digital sales represented 59% of our Q2 revenue, with approximately two-thirds of those sales coming from our own digital channels.

We continue to work every day to improve our operations. Restaurant-level margin of 20.4% in the second quarter was the result of strong operational execution and our cross-functional focus to identify a wide range of process optimization. This includes better labor deployment as well as improvements in supply chain sourcing, which we see continuing into future quarters.

We remain committed to identifying additional opportunities to enhance our restaurant margins. We balance strong revenue growth and restaurant level profit performance with a focus on cost discipline that yielded a reduction in both absolute and relative G&A expenses when compared to the prior year.

Executive Summary

Walmart shares are poised to trade lower despite the company raising its full year sales and earnings guidance from the previous quarter. The equity fell -2.24% after the earnings call, with investors likely underwhelmed by the level of margin recovery the company expects going into the second half of this year. The guidance revision is a function of higher-than-expected sales in the second quarter, and continued sales strength going into the third quarter led by general merchandise categories and grocery

Second Quarter Highlights

Consolidated revenue of $161.6 billion, up 5.7% or 5.4% in constant currency

Consolidated gross margin rate up 50 bps on lapping elevated markdowns and supply chain costs, partially offset by ongoing mix pressure in grocery and health & wellness

Consolidated operating expenses as a percentage of net sales grew 33 bps

Consolidated operating income up $0.5 billion, or 6.7%, adjusted operating income up 8.1%

ROA at 5.6%; ROI at 12.8%, negatively affected by 140 bps of discrete charges in Q3 & Q4 of FY23

Global advertising business grew approximately 35.0%

Walmart U.S. comp sales up 6.4%; eCommerce up 24.0%, led by pickup & delivery

Celebrating the 65th anniversary of Bodega Aurrera stores in Mexico

“We had another strong quarter. Around the world, our customers and members are prioritizing value and convenience. They’re shopping with us across channels — in stores, Sam’s Clubs, and they’re driving eCommerce, which was up 24% globally. Food is a strength, but we’re also encouraged by our results in general merchandise versus our expectations when we started the quarter. Our associates helped deliver increases in transaction counts and units sold, and profit is growing faster than sales. We’re in good shape with inventory, and we like our position for the back half of the year.”

Doug McMillion — President and CEO, Walmart

10% OF ALL BLUE ROOM REVENUES GO DIRECTLY TO FUND OUR NON PROFIT TOGETHERISM.

WE CAN ACCOMPLISH ANYTHING TOGETHER.

These materials do not purport to be all-inclusive or to contain all the information that a prospective investor may desire in considering an investment. These materials are intended merely for preliminary discussion only and may not be relied upon for making any investment decision. Any discussion or information contained in this presentation does not serve as a receipt of, or as a substitute for, personalized investment advice from Blueroom or your advisor.

This publication does not constitute an offer to sell or a solicitation to buy any securities in any fund, market sector, strategy or any other product. Investing is speculative and involves substantial risks (including, the risk of loss of the investor’s entire investment). Past performance is not indicative of future results, and there can be no assurance that the future performance of any specific investment, investment strategy, or product will be profitable.

For more information about us and our general disclosures contact us directly.