Weekend Update #138

Welcome to Blue Room's Weekend Update. Each week, we're sharing what companies we're researching and the what, the who and the how that we think makes the companies interesting and unique. This roundup is brought to you weekly by a group of interns, creative minds, artists and investors who believe that through best in class investing along with the democratization of financial education we can do great things together. Enjoy, Explore and Share.

The S&P 500 equity index fell -2.27% over the week as earnings and economic moves exercised significant influence over markets broadly. The S&P 500 index began the week positive, ending the month of July, closing at a 16 month high Monday. In Japan, the central bank announced an unscheduled bond-purchase operation to tamp down rates following a policy yield move that allows yields to climb to 1.0%. On Wednesday the S&P had its worst day in four months after a U.S. credit downgrade by Fitch Ratings. Treasury 10-year yields hit the highest levels since November causing the dollar to rise. On Thursday, jobless claims data showed resilient demand for workers, while a separate measure showed that labor productivity increased the most since 2020. Finally, to close out the week, payrolls grew 187,000, less than forecast and the second lowest MoM readout since December 2020, while the unemployment rate fell to 3.5% from 3.6%.

This week also set the stage for some of the largest companies in the S&P index to round out the earnings season. On Tuesday, Uber stock fell despite reporting the first operating profit in its history. Some investors were skeptical on the future pace of Uber’s topline. Also on Tuesday, AMD whipsawed, trading up in after-hours trading by over 6.0% and falling by the same clip the following trading day as traders digested the implications of the company’s guidance on AI revenues. On Wednesday, Shopify reported sales and profit beats on greater uptake in core payment solutions, offset by future profitability headwinds as the company’s market matures. On Friday, Apple fell nearly 5.0% on slower-than-anticipated iPhone sales, while Amazon gained more than 8.0% bullish revenue forecast.

Weekly Performance

S&P 500 4,478.03 -2.27%

Dow Jones 35,065.62 -1.11%

Nasdaq 13,909.24 -2.85%

Key Economic Readouts This Week

S&P Global US Manufacturing — Actual: 49.0; Estimate: 49.0; Prior: 49.0

ISM Manufacturing — Actual: 46.9; Estimate: 46.4; Prior: 46.0

ADP Employment Change — Actual: 324k; Estimate: 190k; Prior: 497k

Durable Goods Orders — Actual: +4.6%; Estimate: +4.7%; Prior: +4.7%

Initial Jobless Claims — Actual: 227k; Estimate: 225k; Prior: 221k

Continuing Claims — Actual: 1,700k; Estimate: 1,705k; Prior: 1,690k

Change in Nonfarm Payrolls — Actual: 187k; Estimate: 200k; Prior: 209k

Unemployment Rate — Actual: 3.5%; Estimate: 3.6%; Prior: 3.6%

Thank you Blue Room Analyst IAN CARTER

Apple reports third quarter results

CUPERTINO, CALIFORNIA — Apple today announced financial results for its fiscal 2023 third quarter ended July 1, 2023. The Company posted quarterly revenue of $81.8 billion, down 1 percent year-over-year, and quarterly earnings per diluted share of $1.26, up 5 percent year over year.

“We are happy to report that we had an all-time revenue record in Services during the June quarter, driven by over 1 billion paid subscriptions, and we saw continued strength in emerging markets thanks to robust sales of iPhone,” said Tim Cook, Apple’s CEO. “From education to the environment, we are continuing to advance our values, while championing innovation that enriches the lives of our customers and leaves the world better than we found it.”

“Our June quarter year-over-year business performance improved from the March quarter, and our installed base of active devices reached an all-time high in every geographic segment,” said Luca Maestri, Apple’s CFO. “During the quarter, we generated very strong operating cash flow of $26 billion, returned over $24 billion to our shareholders, and continued to invest in our long-term growth plans.”

Apple’s board of directors has declared a cash dividend of $0.24 per share of the Company’s common stock. The dividend is payable on August 17, 2023 to shareholders of record as of the close of business on August 14, 2023.

Financial Highlights for Second Quarter 2023:

Gross Bookings grew 16% year-over-year (“YoY”) to $33.6 billion, or +18% on a constant currency basis, with Mobility Gross Bookings of $16.7 billion (+25% YoY, or +28% YoY constant currency) and Delivery Gross Bookings of $15.6 billion (+12% YoY, or +14% YoY constant currency). Trips during the quarter grew 22% YoY to 2.3 billion, or approximately 25 million trips per day on average.

Revenue grew 14% YoY to $9.2 billion, or 17% on a constant currency basis.

Income from operations was $326 million, up $1.0 billion YoY and $588 million quarter-over-quarter (“QoQ”).

Net income attributable to Uber Technologies, Inc. was $394 million, including a $386 million benefit (pre-tax) primarily due to net unrealized gains related to the revaluation of Uber’s equity investments.

Adjusted EBITDA of $916 million, up $552 million YoY. Adjusted EBITDA margin as a percentage of Gross Bookings was 2.7%, up from 1.3% in 2Q 2022. Incremental margin as a percentage of Gross Bookings was 12.2% YoY.

Net cash provided by operating activities was $1.2 billion and FCF (CFO - CAPEX) was $1.1 billion.

Unrestricted cash, cash equivalents, and short-term investments were $5.5 billion at the end of the second quarter.

Forward Guidance

Q3’23

Revenue: ~$100 M+

Consensus: $101.0 M

Blue Room: $103.8 M

GAAP operating loss: ($8.0) M

Consensus: ($14.8) M

Blue Room: ($11.0) M

Adjusted EBITDA: $2.0 M

Consensus: $1.6 M

Blue Room: $4.2 M

Full-year 2023

Revenue: mid-single digit percent decline — unchanged

Consensus: -5.8% Y/Y

Blue Room: -4.1% Y/Y

GAAP operating loss: ($19) M - ($14) M — $36M improvement

Consensus: ($48.3) M

Blue Room: ($36.3) M

Adjusted EBITDA: $10 M - $15 M — increased $5M

Consensus: $7.2 M

Blue Room: $16.1 M

Earnings Release Commentary

Caterpillar Inc. announced second-quarter 2023 sales and revenues of $17.3 billion, a 22% increase compared with $14.2 billion in the second quarter of 2022. The increase was primarily due to higher sales volume and favorable price realization.

Operating profit margin was 21.1% for the second quarter of 2023, compared with 13.6% for the second quarter of 2022. Adjusted operating profit margin was 21.3% for the second quarter of 2023, compared with 13.8% for the second quarter of 2022. Second-quarter 2023 profit per share was $5.67, compared with second-quarter 2022 profit per share of $3.13. Adjusted profit per share in the second quarter of 2023 was $5.55, compared with second-quarter 2022 adjusted profit per share of $3.18. Second-quarter 2023 and 2022 adjusted operating profit margin and adjusted profit per share excluded restructuring costs. Second-quarter 2023 adjusted profit per share also excluded a discrete tax benefit to adjust deferred tax balances.

For the first half of 2023, enterprise operating cash flow was $4.8 billion, and the company ended the second quarter with $7.4 billion of enterprise cash. In the quarter, the company repurchased $1.4 billion of Caterpillar common stock and paid dividends of $0.6 billion.

“I’m proud of our global team’s strong operational performance in the second quarter. Our results reflect continued healthy demand as we achieved double-digit top-line growth and record adjusted profit per share while generating strong ME&T free cash flow,” said Jim Umpleby, Chairman and CEO. “Our team remains committed to serving our customers, executing our strategy and continuing to invest for long-term profitable growth.”

Recent Press Releases and Business Updates

June 11, 2023 – Intellia Therapeutics today announced updated interim results from the Phase 1 portion of the ongoing Phase 1/2 study of NTLA-2002. Across all patients (n=10), a 95% mean reduction in monthly attack rate was observed after a single dose of NTLA-2002 through the latest follow-up. At each dose level tested, a robust level of HAE attack rate reduction was achieved. Importantly, the elimination of HAE attacks was found to have been sustained and long lasting. All three dose levels have been well tolerated and the majority of adverse events were mild in severity.

June 5, 2023 – Intellia Therapeutics today announced that Jean-François Formela, M.D. is retiring from its Board of Directors, effective June 15, 2023. Dr. Formela was a co-founder of Intellia and has served as a member of the board of directors since May 2014.

May 31, 2023 – Intellia Therapeutics today announced the acceptance of a late-breaking abstract from the Phase 1 portion of the ongoing NTLA-2002 Phase 1/2 study for a presentation at the European Academy of Allergy and Clinical Immunology (EAACI) Hybrid Congress 2023. The presentation will include updated safety and efficacy results from the Phase 1 portion of the study across all three dose cohorts (25 mg, 50 mg, and 75 mg).

++ Icebreaker Question ++

Since 2000, Warren Buffett has auctioned off a charity lunch with himself, The Oracle of Omaha. Winning bids exceed $1 million, and the 2022 lunch is reported to have sold for $19 million. Wow!

Imagine that you are invited to an intimate lunch with the industry icon of your dreams: Elon Musk, Taylor Swift, Christine Lagarde, President Obama, Oprah Winfrey, Jen-Hsun Huang, Carlos Slim, Eminem, etc.

1. Who would you choose, and why, and what is the lunch setting?

2. How would you present yourself?

3. If you had a request for this person, how would you approach making a successful ask?

PLEASE ENJOY COMMENTARY FROM OUR

BLUE ROOM FELLOW

— LEXI LINAFELTER —

Industry Icons:

Who else but Dolly Parton?

I have had the honor to live the better half of my college career with a Dolly Parton superfan. Consequently, Dolly was the first to come to mind as a unique but relatable figure, absolutely EPIC guitar player, and fabulously complex role model for any young woman. Simply stated, lunch with her would be a masterclass in authenticity.

Sitting across from Dolly at lunch to talk country music, guitars, and dissect her beautifully outsized aesthetic would be life-changing on its own. I would, however, be more interested in her insight into living genuinely and confidently, distilling from her lighthearted disposition what it means to allow every element of one's character to show in its entirety.

Beyond her revolutionary discography, her work is unifying across geographic, political, and socioeconomic lines; from humble Appalachian beginnings to the Rock and Roll Hall of Fame, as a philanthropist and a feminine role model, she moves gracefully and intentionally. She contributes to communities she is close to and speaks passionately on issues she believes in, all while maintaining a vastly diverse and immensely loyal fan base. Dolly has won over the public eye as herself, unapologetically. Out of respect for her as a musical legend and THE “cool girl,” I would have to do the same.

If you are as interested in Dolly’s impact as I have recently become, check this out as a start: https://twitter.com/CalltoActivism/status/1673757904829050880?t=vUxVlKto429hiZOSlhBFLA&s=01

Thank you Blue Room Fellow LEXI LINAFELTER

For more Blue Roomer answers, please view this week’s GLOBAL meeting below.

Executive Summary

Yelp shares are positioned for continued growth in 2H 2023 as the company incorporates neural networks and Large Language Models (LLMs) into its tech stack which continue to increase value for both advertisers and consumers alike. In 2022, Yelp posted ~16% growth and so far this year, although revenues have stabilized at 13%, Yelp has expanded advertising revenue per location for four straight quarters and its AI-enabled ad stack will help carry this trend into 2024 as well.

Valuation

2023 EPS: 45.5x $1.00 expected

2024 EPS: 26.7x $1.70 expected (+70% growth)

Details

Yelp's growth in advertising revenue accelerated 14% in the second quarter of 2023 to $322 million, up from 13% in the preceding quarter. This growth was fueled by accelerating revenue in both the Services and Restaurant, Retail & Other segments, which themselves saw expanding advertising revenue location growth of 12% and 16% year-over-year, respectively. This contributed to overall advertising revenue per location of $571.89—a record—on a base of 563,000 locations which remained relatively flat year-over-year. Advertisers are willing to pay more for Yelp's ad stack, which they are increasingly upgrading with machine learning and LLM capabilities to further increase its value proposition to both advertisers and consumers alike. Yelp is able to do this while pruning operating expense, managing to reduce it by ~2% sequentially as it removed costs from sales and marketing and further plans to reduce stock-based compensation to 8% of revenue by 2025. This resulted in operating margin of 5.6% in the quarter, a 20-basis-point improvement from the same year-ago period, and adjusted EBITDA margin of ~25%, which increased by 240 basis points year-over-year. Yelp has positioned itself as a worthwhile advertising platform whose only risks it seems stem from systematic rather than unsystematic risk (i.e., macroeconomic uncertainty that may adversely impact advertising budgets in the future).

Executive Summary

Coinbase continues to demonstrate its strong brand and reputation as it maintains higher trading fees compared to other industry players, while also gaining market share in global spot volume. Subscription and Services revenue (50.6%) exceeded Transaction revenue (49.4%) for the first time in the company’s history, showing the success in Coinbase’s efforts to diversify its business. The company is also demonstrating its ability to operate efficiently with a 12.8% sequential reduction in OpEx (58% reduction Y/Y), achieving adjusted EBITDA positive for the second quarter in a row. The company is poised to be a major benefactor of pending crypto legislation, and with new product rollouts and international expansion, COIN likely has significant upside potential going into 2024.

Earnings Call Notes:

Guardant continues to anticipate their improved Shield algorithms to improve sensitivity, especially among advanced adenoma cases, will only require a supplemental approval from the FDA shortly following approval of Shield

Lung and breast cancer indications drove strong growth in Guardant360 volume during the quarter

Both Reveal and TissueNext volumes continue to grow

August 3, 2023 BLUE ROOM Meeting #121

Thursday

August 3, 2023

12 PM

BLUE ROOM

MEETING NUMBER

121

__________

Icebreaker Question:

Since 2000, Warren Buffett has auctioned off a charity lunch with himself, The Oracle of Omaha. Winning bids exceed $1 million, and the 2022 lunch is reported to have sold for $19 million. Wow!Imagine that you are invited to an intimate lunch with the industry icon of your dreams: Elon Musk, Taylor Swift, Christine Lagarde, President Obama, Oprah Winfrey, Jen-Hsun Huang, Carlos Slim, Eminem, etc.

1. Who would you choose, and why, and what is the lunch setting?

2. How would you present yourself?

3. If you had a request for this person, how would you approach making a successful ask?

Three Years Ago

. . .

Meeting #12

July 30, 2020

Recent Press Releases and Business Updates

July 10, 2023 – FierceBiotech reported preliminary formulations for Moderna and Merck’s Phase 3 trial for its individualized neoantigen therapy. The study will stretch the patient population to include individuals with Melanoma as early as stage 2b. The trial, code-named V940-001, is expected to enroll 1,089 patients and has a primary completion date set for October 2029.

July 5, 2023 – A Moderna spokesperson notified CNBC that Moderna struck a deal with Chinese officials to research, develop and manufacture mRNA medicines in the country. The drugs would be “exclusively for the Chinese people” and won’t “be exported.” It was further reported by Chinese media outlet Yicai that Moderna was slated to make its first investment in China that could be worth around $1 billion, citing unnamed sources. It was also reported that Moderna CEO Stéphane Bancel was visiting Shanghai around the time that the news broke.

July 5, 2023 – Moderna today announced that it has submitted marketing authorizations for mRNA-1345, a vaccine for the prevention of RSV-associated lower respiratory tract disease (RSV-LRTD) and acute respiratory disease in adults aged 60 years or older, with the European Medicines Agency (EMA), Swissmedic in Switzerland, and the Therapeutic Goods Administration (TGA) in Australia and has initiated the rolling submissions process for a BLA to the U.S. FDA. mRNA-1345 received Breakthrough Therapy Designation and was previously granted Fast Track designation by the FDA.

July 3, 2023 – Moderna today announced that it has submitted a regulatory application to the European Medicines Agency (EMA) for its updated COVID-19 vaccine encoding the spike protein for the XBB.1.5 sublineage of SARS-Cov-2.

Ex Vivo Allogeneic CAR T Platform

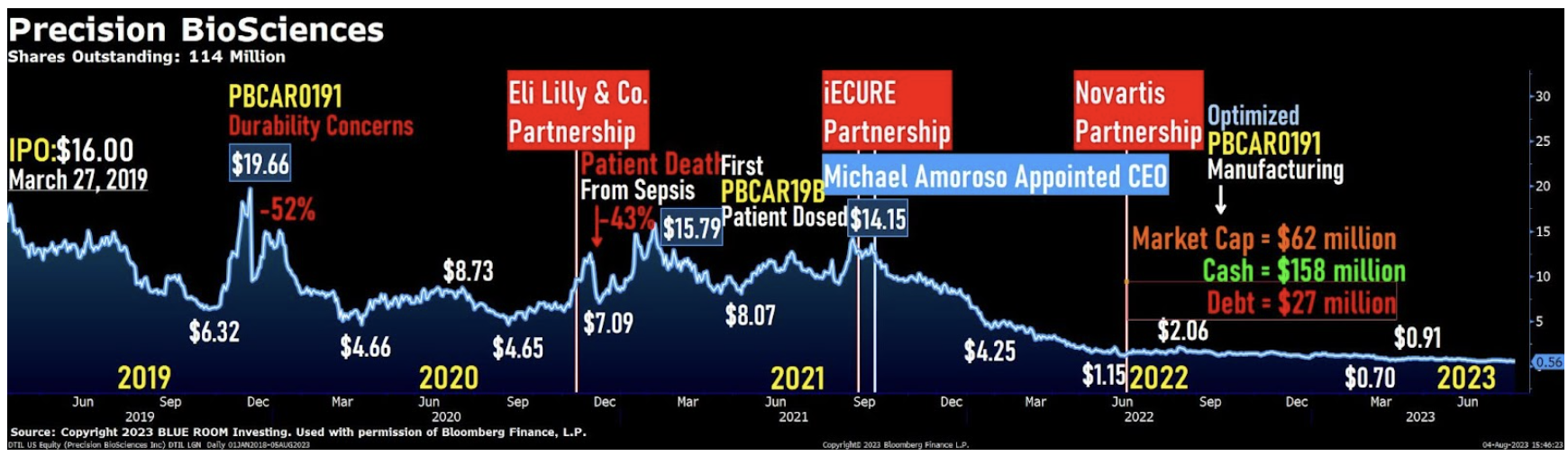

In July 2023, Precision received final meeting minutes from its June 2023 Type B meeting with the FDA for azer-cel. The objective of the meeting was to gain further clarity on the potential registration path for azer-cel including study design, endpoints, and the recommended phase 2 dose in the CAR T relapsed patient setting. The discussion with the FDA provided clarity on azer-cel development, including potential pathway toward registration. Based on the advice received from the FDA and clinical data shared during the May 2023 CAR T update, Precision is currently advancing discussions with multiple potential strategic partners for its cell therapy assets, including hematologic and non-hematologic applications.

In Vivo Gene Editing Platform

ARCUS may have broad utility in many diseases and the company believes ARCUS is uniquely suited for in vivo gene editing, including the potential to produce a profound impact on diseases that are best treated by therapeutic gene insertion or excision of large defective gene sequences.

Executive Summary:

In Q2 2023, Nutrien suffered from industry-wide lower realized prices for fertilizer across all three nutrients that was somewhat offset by higher volumes sold across all three nutrients.

Non-cash impairments to LatAm retail and White Spring phosphate assets tanked EPS, bringing it from $2.53 to $0.89.

Outlook for the second half of the year is very strong in North America, driven by high demand for fertilizer, a longer projected fall application window, and tighter supplies of potash and ammonia. Offshore outlook is thought to be weaker than expected, causing a reduction in forward guidance for the second half of the year.

Strategic cost cutting actions include the suspension of a potash production ramp-up, the cancellation of the Geismar clean ammonia plant, and reduced new investments in Brazil. These cost cuts appear wise given the volatility in crop input markets, especially in Brazil, and allow Nutrien to focus on low-cost operations and integration of their 9 Brazilian retail businesses that were acquired in the last 3 years.

Business Updates

Cystic Fibrosis (CF) Marketed Products

Approval from the European Commission for the use of ORKAMBI in children with CF ages 1 to <2 years old who have two copies of the F508del mutation in the CFTR gene. With this approval, approximately 300 children with CF are eligible for the first time for a medicine that can treat the underlying cause of their disease.

At the European Cystic Fibrosis Society’s (ECFS) European Cystic Fibrosis Conference in June, Vertex presented interim results from the largest real-world study of TRIKAFTA/KAFTRIO, which showed sustained improvement in lung function, reduction in pulmonary exacerbations frequency and lower rates of lung transplant and death for people with CF.

Approval from the U.S. Food and Drug Administration (FDA) for the use of KALYDECO in children with CF from 1 month to <4 months of age. This approval represents the first and only CFTR modulator approved for this age group. Vertex also submitted Marketing Authorization Applications (MAAs) to the European Medicines Agency (EMA), the Medicines and Healthcare products Regulatory Agency (MHRA) in the United Kingdom, and Health Canada for the use of KALYDECO in children with CF from 1 month to <4 months of age.

Approval from the FDA for the use of TRIKAFTA in children 2 to 5 years of age with at least one F508del mutation in the cystic fibrosis transmembrane conductance regulator (CFTR) gene or a mutation in the CFTR gene that is responsive to TRIKAFTA. With this approval, approximately 900 children are eligible for TRIKAFTA for the first time. Vertex also completed regulatory submissions with the EMA, the MHRA, Health Canada, and the Therapeutic Goods Administration in Australia for the use of KAFTRIO/TRIKAFTA in children 2 to 5 years of age.

Executive Summary

Shopify exceeded expectations for Q2 2023 revenue and earnings on an adjusted basis during a period of uncertainty about the durability of consumer spending while also seeing great adoption of its core payments solutions and attach rates. However, the expense savings outlook was clouded after high expectations for the impact of the sale of the fulfillment business last quarter, and profitability will be more challenged than previously expected. Compounding the expense and profitability overhang is a lack of concrete long-term guidance about how Shopify can sustain such high merchant and revenue growth rates given the rapid market penetration they’re already achieving. The macroenvironment could certainly deteriorate rapidly due to a number of risk factors, but currently, financials continue to show better-

Paul Hennessy — CEO

Thank you, Chris. Hello everyone, and thank you for joining us today. I'm thrilled to walk through Shutterstock's second quarter with you this morning, as there are some extremely exciting developments in our business.

Before going into the details, I'd like to start by providing a bit of context back at our Investor Day in February. We talked in depth about our Content, Creative and Data engines and the massive opportunities we see driven by step-change innovations such as generative AI. And we also spoke about the potential for Creative and Data to become a more important part of our overall revenues.

I'm pleased to report that as reflected in our second quarter results in our revised full year outlook, Shutterstock is not only adapting, but it is thriving in this dynamic environment. We are signing industry-shaping AI data partnerships. We acquired GIPHY to lead the way in moment marketing and conversational content, and we are embracing a culture of rapid and iterative experimentation when it comes to managing our content business.

At the same time, having achieved record revenue in EBITDA on a year-to-date basis, I'm pleased to report that we are increasing our guidance on top- and bottom-line for the full year 2023. In addition, beginning today, we will be breaking out the revenue derived from our Data Engine.

Executive Summary

Schrödinger demonstrated the strength of the underlying software business and confidence in conversations about large customers further stepping up large-scale deployment in 2023 by raising software revenue guidance, yet the discontinuation of development of a candidate from the Zai Lab collaboration produced an overhang for SDGR shares. Over the short-term and long-term, the impact of Zai Lab abandoning development is minimal on Schrödinger’s revenue trajectory, as the collaboration included an estimated $320 million remaining in potential milestone payments to be spread over time through 2029, if successfully commercialized. However, Schrödinger was expected to have a good chance of announcing a new collaboration during the year as opposed to having one discontinued. Management will have the choice to partner or pursue internal development to further monetize the asset, but it seems that the overall strategy is shifting toward internal development vs. collaborations to achieve the best risk-weighted returns on investment. $20 million in milestone payments expected during 2023 are also being shifted to 2024, which further places weight on continued success over 2024 to reaccelerate software revenue from 16.5% YoY to 24.0% YoY and drug discovery revenue from 34.9% YoY to 129.8% YoY.

Recent Press Releases and Business Updates

July 27, 2023 – Editas Medicine and Azzur Cleanrooms on Demand (COD), an Azzur Group Company, today announced the companies have expanded their multi-year contract to support the scaling of EDIT-301. The agreement includes compliant cleanroom space and lab services at Azzur’s COD site in Devens, Massachusetts. Editas has utilized Azzur’s services to execute preclinical and early-phase clinical manufacturing activities for its cell medicines, including EDIT-301 for the treatment of sickle cell disease and beta thalassemia, since 2020.

July 26, 2023 – Editas Medicine today announced that it will host a conference call and webcast on Wednesday, August 2, 2023, at 8:00 a.m. ET.

July 25, 2023 – Editas Medicine today announced the grant of an inducement award to the Company’s new CSO, Linda C. Nurkly, Ph.D. The stock option provides for the purchase of up to 135,500 shares of Editas Medicine common stock at a price of $8.66 per share.

July 24, 2023 – Editas Medicine today announced the appointment of Linda C. Burkly, Ph.D., as the Company’s Executive Vice President and Chief Scientific Officer. Prior to joining Editas, Dr. Burkly held positions of increasing responsibility over a 37-year tenure at Biogen, most recently leading neuroscience-focused research teams as Vice President and Senior Distinguished Investigator.

June 14, 2023 – Editas Medicine today announced the pricing of an underwritten offering of 12,500,000 shares of its common stock at a public offering price of $10.00 per share.

June 14, 2023 – Editas Medicine today announced that it intends to offer and sell $125 million shares of its common stock in an underwritten public offering.

Executive Summary

Despite almost every metric being a beat and raise in Q2 by Exact, EXAS stock traded down after hours at $91.50 (-5.1%). The raised full year guidance would imply a ~15% YoY growth rate for revenue in H2 2023 whereas H1 2023 has already shown a ~22% YoY growth rate. This type of conservative guidance is exactly what has hurt EXAS stock at past earnings calls and investor presentations. The investors is, “If you are doing so well, why does your guidance imply deceleration?” However, most instances of this negative reaction to beat and raise performance have all been short-lived downticks as the underlying results are showing really strong performance of Cologuard and Exact’s financials, and CFO Jeff Elliott is known for these conservative, high-likelihood estimates while improving the underlying financials.

Executive Summary

Amazon shares are poised to gain in the 2H 2023 as the company sees reacceleration in its AWS business and makes improvements in its fulfillment network productivity and operating leverage and benefits from moderating inflationary pressures. In 2022, Amazon posted ~9% growth and so far this year, revenues are increasing 10% and are positioned to accelerate into 2024.

Valuation

2023 EPS: 79.2x $1.76 expected

2024 EPS: 65.6x $2.13 expected

Details

Amazon posted Q2 2023 revenue of $134.4 billion, growing 10.8% year-over-year and representing an acceleration from the 9.4% year-over-year growth seen in the previous quarter. This was driven by a rebound of sorts in its AWS business where customers are shifting from cost optimization to "new workloads, new business." This was reflected in AWS revenue of $22.14 billion, growing 12% year-over-year and poised to reaccelerate—Amazon highlighted new functionality in generative AI, large language models and machine learning that will result in future growth, saying "[we're] optimistic and starting to see some good traction with customers' new volumes." Amazon saw a reacceleration in Online Stores and Advertising Services as well, each growing 4.2% and 22%, respectively. The company provided a Q3 2023 revenue guidance range of $138 billion to $143 billion, representing 10.5% year-over-year growth at the midpoint and itself an acceleration from the previous quarter. Further, the company provided operating income guidance of $5.5 billion to $8.5 billion reflecting operating leverage resulting from optimization in its fulfillment network designed to provide same-day and next-day delivery for regions' top 100,000 SKUs at lower transportation costs and less "touches" along the supply chain. Shares rose as high as 11.4% before settling at $139.57 indicating investors were pleased with the progress Amazon has been making across its business.

10% OF ALL BLUE ROOM REVENUES GO DIRECTLY TO FUND OUR NON PROFIT TOGETHERISM.

WE CAN ACCOMPLISH ANYTHING TOGETHER.

These materials do not purport to be all-inclusive or to contain all the information that a prospective investor may desire in considering an investment. These materials are intended merely for preliminary discussion only and may not be relied upon for making any investment decision. Any discussion or information contained in this presentation does not serve as a receipt of, or as a substitute for, personalized investment advice from Blueroom or your advisor.

This publication does not constitute an offer to sell or a solicitation to buy any securities in any fund, market sector, strategy or any other product. Investing is speculative and involves substantial risks (including, the risk of loss of the investor’s entire investment). Past performance is not indicative of future results, and there can be no assurance that the future performance of any specific investment, investment strategy, or product will be profitable.

For more information about us and our general disclosures contact us directly.