Weekend Update #118

Welcome to Blue Room's Weekend Update. Each week, we're sharing what companies we're researching and the what, the who and the how that we think makes the companies interesting and unique. This roundup is brought to you weekly by a group of interns, creative minds, artists and investors who believe that through best in class investing along with the democratization of financial education we can do great things together. Enjoy, Explore and Share.

+ 2023 +

SPRING BREAK

DOUBLE FEATURE

Following market turmoil last week as the closure of SVB spooked depositors across the banking sector, markets managed to end the week positive as the FDIC and Treasury stepped in to guarantee all deposits, preventing further contagion to other banks. Signature Bank wasn’t very fortunate, the announcement came the same time New York State regulators decided to close Signature Bank. While the contagion is mostly contained, banks were still under stress as First Republic Bank needed $30 billion from a group of 11 financial institutions including Bank of America, Wells Fargo, Citigroup and JPMorgan Chase. Credit Suisse also needed to borrow $54 billion from Switzerland’s central bank.

Crypto surged this week as the banking crisis highlighted flaws of traditional banking and fractional reserves, supporting a case for a decentralized and transparent monetary system.

Markets will be closely watching the Fed’s rate hike decision next week, as well as Chair Powell’s commentary regarding the direction future rate decisions.

Friday’s Close (Weekly Performance)

S&P 500 3,916.64 1.43%

Nasdaq 11,630.51 4.41%

Dow Jones 31,861.98 -0.15%

Thank you Blue Room Analyst NICK PEART

Dear Newsletter Reader:

Is the failure of Silicon Valley Bank an idiosyncratic tragic event, brought on by the

bank’s overconcentration to America’s capital markets dependent startup economy,

or is SVB’s demise the canary in the coal mine for the broader banking industry?

As of December 31, 2022, 55 Offices, 8,553 employees // Total Assets: $212 Billion // Total Equity: $16 Billion

January 19, 2023 : $250.04 | SIVB holds Q4 2022 Earnings conference Call

February 2, 2023 : $333.50

Friday, March 10, 2023: Trading Halted, Silicon Valley Bank closed.

Monday, March 13, 2023, all insured deposits will be available for bank customers.

So what went wrong so fast? And what does it mean for your investment portfolio?

Leading up to the FY2023 Q4 earnings call, the company had recently announced a second reduction in force of 10%, with a significant amount of the plan concentrated in sales and marketing.

DocuSign’s quarterly earnings results exceeded expectations, with total revenues of $660 million and adjusted diluted EPS of $0.65 versus consensus estimates of $640 million and $0.52, respectively. Similarly, DocuSign’s fiscal year earnings results also exceeded expectations, with total revenues of $2,516 million and adjusted diluted EPS of $2.03 beating estimates of $2,496 million and $1.92, respectively.

The company released Q1 FY2024 guidance, which missed street estimates on both the revenue and billings fronts and issued Fiscal Year 2024 guidance which also missed revenue expectations and underwhelmed on billings. The stock reacted according, falling as low as 20% in the trading following the earnings release and conference call. The following are key takeaways and highlights from the latest earnings results:

“While we are pleased with our Q4 results, I also want to acknowledge today’s challenging macro environment. Customer sentiment continues to be cautious, and that is reflected in moderated expansion rates.”

Chief Financial Officer Cynthia Gaylor has decided to step down from her role. She will remain with the company through the first quarter of the 2024 fiscal year

“We are already leveraging sophisticated AI models for contract analysis and automation of some workflows, and we’re very excited to harness generative AI, data and pattern identification as yet another way we can increase productivity, reduce friction, and save our customers’ time.”

The company is emphasizing product-led growth (where user acquisition, expansion, conversion and retention are all driven primarily by the product itself) and self-serve (an approach where users access resources to find solutions on their own without requiring assistance from a service representative)

The recent workforce reductions were in the sales organization, and part of the cost savings from these decisions are being reinvested in product development and innovation

Blue Room Analyst Takeaways

Nvidia has committed to serving various types of customers seeking to use accelerated computing in their AI infrastructure. They serve these customers at various levels as well, which includes total software development, partial software development, access to vGPU servers, access to physical hardware servers, and Nvidia AI-as-a-Service bundled.

Regarding the outlook and the indicated slowdown of corporate expenses across the board, Nvidia considers its solutions as immune to CAPEX cuts.

The company indicates that it tends to be “front and center” of the priority list even as expenses are cut. They are not immune to pushouts, however, indicating potential volatility in revenue as a result.

This can also be exacerbated by cloud services providers facing their own infrastructure supply chain headwinds, which impact H100 ramp due to newer PCIe, softwares, etc.

The company expects quarterly acceleration of the YoY growth rate in every quarter this year.

Nvidia has worked with OpenAI for a number of years, so the evolution of GPUs is indicative of what developers are working to bring to market in the future.

According to the conference call, the way that Nvidia recognizes “AI-as-a-Service” revenue is by charging a subscription fee above the rate that it pays CSPs for hosting the instances.

We should start contextualizing AI models as a commodity going into the future according to the way that Nvidia, and others, talk about them.

CSPs have their own models but Nvidia’s models won’t be competitively challenged by them.

Nvidia’s models are designed to optimize performance on GPUs generally, and less end-result specific.

Gaming is likely to accelerate in Q1 on the inventory correction meaning that growth in the segment on a full year basis is likely.

Nvidia alluded to a stronger back half of the year from a sales perspective

We should look at the Mercedes x Nvidia partnership as the ideal automotive business model for Nvidia DRIVE platform.

Blue Room Analyst Takeaways

Representatives from Generate Biomedicines and Nanostring Industries (NASDAQ: NSTG), two healthcare companies that Nvidia has partnered with, were panelist:

Generate Biomedicines: Uses ML and AI to discover proteins and apply those proteins to potential disease indications for drug discovery. private

Nanostring Industries: Offers tools to discover the underlying functions and relationships of proteins to allow researchers to understand the root causes of complex diseases such as cancer. public.

Our overall takeaway is that Nvidia is offering acceleration libraries that are better in aggregate (e.i. when combining GPUs, DPUs, Nvidia CPUs, and softwares) than current solutions by “orders of magnitude”, in terms of performance acceleration. Competitive solutions are primarily Intel and AMD’s x86 architecture-based server processors.

Nvidia’s overall value proposition is to allow drug discovery companies to increase their likelihood of pre-clinical and clinical trial success by leveraging AI to predict those outcomes.

The advancements in biologics discovery is not at it’s full economies of scale potential because it is road blocked by inaccuracy in trials and failures along the way. This results in essentially wasted R&D that could have been used for other investigational drugs that have higher probabilities of success.

There were nine references to ChatGPT on the call. ChatGPT was used as an example in this session as a precursor to what is possible on a marketable level with deep learning. Both conversational AI and genomics models are generative AI natural language processing (NLP) models, however the model inputs are slightly different because the outputs are different. We see the market broadly adopting the revolutionary possibilities of generative AI, but primarily focusing on art and conversational end-markets. To us, the actual scope is much broader and includes genomics, weather forecasting, predictive modeling, and recommender systems. We believe that these additional use-cases extend the go-to-market ability of generative AI, which ultimately expands Nvidia’s addressable markets.

Alan Blinder’s review of economic policy over the past 60 years should be required reading for anyone hoping to understand the history of economic thought in the United States and its impact on the actions taken by Federal Reserve officials. While firmly Keyesian in his approach, Blinder provides the foundation for understanding the impact of academic economists’ role in influencing monetary policy. What’s more, Blinder details the outsized importance of political economics and fiscal policy in shaping the economic landscape – whether or not it be in accord with monetary policy. In a year in which many economic and financial analysts are looking to the past as a way to foretell the future, Blinder’s narrative – especially that surrounding the stagflationary era of the 1970’s – is a prudent place to start.

Benjamin Swinburne — Analyst, Morgan Stanley

So I thought we could organize our conversation around sort of the three phases of growth that you guys talk about when thinking about your -- and discussing your business model. So that's really around scale, engagement, and monetization. Maybe starting with the scale of the business, can you talk a little bit about the audience that Roku reaches today, and how you expect to grow that over time?

Anthony Wood — Founder, Chairman and Chief Executive Officer

Sure. So Roku just passed 70 million active accounts, which is kind of a proxy for a household for us. We added 10 million net new active accounts last year, which was a big year for us, it's the biggest year, it's the most active accounts we've added in any year since -- except for 2020, which was sort of the height of the stay-at-home boost that we got. And that's a combination of international and U.S. Roku is a global TV OS. And the market share -- our market share continues to grow in all the countries that we're active in and there's a lot of growth ahead I think in terms of active accounts.

Benjamin Swinburne — Analyst, Morgan Stanley

You talk a lot about the operating system as being sort of one of the core drivers of market share gains. We've seen some of the big TV OEMs like Samsung and LG continue to invest in their own operating systems. Talk about what differentiates the Roku OS, and why that's driving market share pick-up around the world?

Anthony Wood — Founder, Chairman and Chief Executive Officer

Yeah. So the -- Roku's basic OS strategy is to build a purpose-built operating system for television. So, it's the same way that back in the day, Windows became the leading operating system for desktops by building a purpose-built platform for that customer and that ecosystem, the way Android became a very popular phone OS, being purpose-built for that platform. And Roku is purpose-built for TV. So that -- by focusing on that particular that -- the TV ecosystem exclusively, we just do a better job. And so the result is that Roku's share is growing. I mean, in the United States last year in Q4, we sold more -- more Roku TVs were sold than Samsung and LG sold combined. So we're the number one platform in lots of countries, including the United States.

Our brand continues to grow. Our brand was named the fastest-growing brand for Gen-Zs. So we're -- the Roku City screensaver, which is our screensaver, it's become an iconic part of our brand and part of our efforts to delight consumers. The Roku City screensaver is mentioned every 12 minutes on Twitter now. So there's a lot of things that go into our continued growth in market share.

Greg Peterson — Head of Investor Relations

(…)Last year at about $12.7 billion in sales, we were the largest pure-play agricultural equipment and precision ag solutions company. Diverse revenue base, about half of it comes from Western Europe, 20% to 25% in North America, 20-ish% South America, and the balance is primarily in Australia and New Zealand.

We're roughly a 30-year-old company put together with over 30 acquisitions over that period of time. Maybe the most significant was the last major acquisition, which was a company called Precision Planting. Some of you may or may not have heard of that, but it arguably was probably the most successful ag tech company we've seen in our industry for sure.

It was very important to AGCO for probably 3 reasons. Number one, it gave us unquestionably probably the best planting technology. Number two, it introduced the concept of retrofit first to our business, and it's one that we've embraced and taken not just planting but across the crop cycle. And number three, it gave us another distribution channel, which is enabling that retrofit strategy and really is a big differentiator between us and our competition.

As a company highly dependent on consumers’ willingness and ability to make big-ticket discretionary purchases, we believe that Thor could see a significant slowdown in sales activity in a recessionary environment as a company boat exposed to a potential decline in consumer demand and carrying costs throughout the value chain. Coming off nearly two years of record sales growth, provided in large part due to a major increase in economic stimulus, alongside a deteriorating macroeconomic backdrop, we believe Thor’s bloated inventories will have to reconcile a significant drop in demand during an economic slowdown, as consumers pull away from large discretionary purchases that are heavily reliant on financing. This poses significant risks to the company’s margins, as promotional activity will likely tick up in response to building inventory. As a final headwind, continually rising interest rates further eat away at both consumer and dealer appetite for making large discretionary purchases and taking on additional inventory, which leaves Thor further exposed to downstream demand destruction.

Quarter results:

Total revenue $4.66 billion, up 9% y/y, 13% in constant currency

Digital Media revenue $3.40 billion, up 9% y/y, 14% in constant currency;

net new Digital Media ARR of $410 millionDigital Experience revenue $1.18 billion, up 12% y/y, 14% in constant currency

GAAP EPS of $2.71 and non-GAAP EPS of $3.80

Q2 Guidance:

Total Adobe revenue of $4.75 billion to $4.78 billion

Digital Media net new ARR of $420 million, Digital Media revenue $3.45 - $3.47 billion

Digital Experience revenue $1.21 billion to $1.23 billion

GAAP tax rate ~21.5%, non-GAAP tax rate 18.5%

GAAP EPS $2.65 - $2.70, non-GAAP EPS $3.75 - $3.80.

Fiscal 2023 guidance

Digital Media net new ARR of $1.70 billion,

GAAP EPS of $10.85 to $11.15 and non-GAAP EPS of $15.30 to $15.60

Adobe had a strong first quarter for 2023, beating upper guidance in the midst of an uncertain economic climate. They attributed their wins to their diverse portfolio of mission-critical products that follows their customer through the whole workflow.

They are seeing strength across the board as companies look to consolidate their applications to improve efficiency.

Adobe is very excited about the potential from their acquisition of Figma that is expected to close by the end of 2023, specifically in product design, collaboration with Photoshop and Illustrator, and its own evolution.

Adobe will be having their Adobe Summit at the Venetian Convention and Expo Center in Las Vegas, beginning on Tuesday, March 21, where they will unveil innovation relating to generative AI and across their Clouds.

BLUE ROOM

GRAIN

Q1 2023 Meeting

Wednesday

March 8, 2023

3 PM

STAY TUNED FOR MORE.

Reshma Kewalramani — Chief Executive Officer and President

Tthank you so much for having us here. It's wonderful to see all of you in person, in our home city of Boston.

To start with, maybe I'll just give you a little bit of a flavor for where Vertex is today, touch on a few of our programs, and then, Phil, we can go into any one of those that you'd like to. It is an extraordinarily exciting time for us at Vertex. Having now brought four CF medicines to market and transformed that disease, the growth in our CF franchise, has transformed Vertex. We are now involved in eight disease areas including cystic fibrosis, those are in the clinic today. And five of those disease areas are now past the proof-of-concept stage.

A few years ago, we would have been talking about a lot fewer programs, but we would have also been talking about a lot fewer modalities. Today, we are, of course, working in small molecules across a number of these disease areas, but we're also working in gene-editing with CRISPR/Cas9, with cell therapy, and our Type 1 Diabetes programs, and with mRNA in our CF programs.

As we've gone through this growth, we've also expanded our footprint right here in Boston. We are at our headquarters in Fan Pier. And just about a mile down the street, we've opened up our second large building, we call it Line 1, we're building Line 2 just across the street to accommodate our growing cell and gene presence.

Brian Armstrong — Co-Founder, Chairman & CEO

Yes. Well thanks for having us here, first of all. And happy to talk about some of the use cases. But I think you laid it out well, 80% of Americans today feel the current financial system is not serving them. So it takes too long. The fees are too high. It's not serving everybody equally. And cryptocurrency is one of those technologies that can really update the financial system.

So whether it's every time you're setting a payment, why isn't it as fast and cheap and global as sending a text message or WhatsApp message, right?

Why is it, that every time you swipe your credit card, you're losing 2% or at least the merchant is. Or similarly, we talk about T+2, T+3, settlement, why can't that be instant and just eliminate an entire category of risk in the financial system. So a lot of these tools that we're using, they're based on code that's 40 years old, running on these cobalt mainframes and the laws are sometimes 100 years old or more. And so cryptocurrency is really a way you can think of it to create new financial infrastructure that's more efficient and global and fair and free.

So you asked about Coinbase's role in this? I mean -- well, we really have -- we have a role to play as the primary financial account for people engaging in the cryptoeconomy using this new technology. And we also have a role to play as the most trusted and compliant player in the space. I think recent events and this increased regulatory scrutiny are really -- I believe, there are going to be a -- there is going to be a net beneficiary of that environment because for the last 10 years, we've been following an approach that is compliant, it is trusted.

Mike Mason — Executive Vice President & President, Lilly Diabetes

Good to see everyone. We’re all packed into a tight room, so hopefully, no one has COVID or else we'll all have it.

But, yes, I know everyone here is excited about obesity and trying to figure out the size of it. Obviously, we're doing the same thing at Lilly and trying to make it as massive an opportunity to help as many patients as possible. It is a chronic disease that really affects both physically, emotionally patients’ lives. We're starting to get into the deep emotional consequences of living with chronic management for a lifetime. And it's quite humbling to think that we have a product that after approval could really help change the lives of people.

Yes, I think it will come down to access. I think if you look at over the last couple of years, you may have been wondering, okay, our health care professional is going to write it or consumer is going to be interested in it. I think those questions have been checked. I think the big question is going to be long-term access in the U.S. By our estimates, and I think by what Novo has said publicly, about half of employers have opted into obesity medications. And so it's growing that as well as trying to get access in Medicare Part D.

Terry Dolan — Chief Financial Officer

Yes. Maybe just kind of very broadly, if you think about — at the end of 2022, inflation was starting to moderate and all sorts of things. I think there were a few surprises, kind of in the January, February time frame with respect to a number of the different indicators. And so I think, what that tells you is that inflation is just something that's very stubborn.

And as a result of that, I think from a Fed policy perspective, being sufficiently restrictive, I think that's going to be their mantra for a while. What that tells us is that maybe in terms of our base case, from an interest rate perspective, we would expect rates to probably continue to move up in the near term, closer to that 550 sort of range, and then probably stay there for a while before starting to come down.

I think kind of earlier this year, there was an expectation that we would move into a recession and rates would start to drop at the end of 2023. And I think that while we would still expect a recession probably to occur, I would say it's — soft landing is not a bad way of describing it, a mild sort of recession, probably at best a moderate recession. But the timing of that is something that I think we're continuing to kind of push out a little bit. If it does occur probably late 2023, early 2024, kind of in that time frame, so that would be kind of a couple of different things.

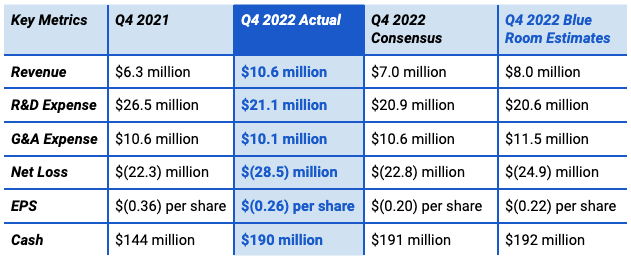

Precision BioSciences’ Q4 2022 earnings updates were largely incremental and in line with expectations. The company surprised to the upside on Q4 revenue as milestone payments stepped up at the end of the year. Full year 2022 revenue from Novartis was $9.5 million and the company recognized $15.6 million in revenue from Eli Lilly.

Net loss was slightly wider than expected as Precision recognized a $10.8 million impairment of prepaid expenses through the other expense line item associated with the company’s decision to pause work on the iECURE PCSK9 collaboration.

The CAR T program update on azer-cel and PBCAR19B has also been delayed again to an updated timeframe of April/May 2023 — which had originally been scheduled for the end of Q4 2022. The upside to this delay is that the company is ensuring they collect adequate long-term patient follow-up in order to set up an End of Phase 1 meeting with the FDA and to discuss moving to a pivotal Phase 2 trial with azer-cel.

Another positive note within the press release was the announcement that Precision would provide additional data on the HBV and DMD programs at an in vivo update in mid-2023. OTC continues to progress to filing a CTA/IND by the end of 2023, which would be Precision’s first in vivo treatment in clinical trials.

BLUE ROOM

+WEEKLY+

THURSDAY’S GLOBAL ZOOM

—

Thursday

March 9, 2023

12 PM

BLUE ROOM

GLOBAL MEETING #110

———————

Agenda

-- Blue Room Investing

-- Blue Room Impact

Icebreaker Question:

The Academy Awards will be presented this Sunday.

-- Which film will win the Oscar for Best Movie and why?

-- You get to choose one movie, which every living American will have to watch, what would it be?

Happy Birthday to Ian, who will celebrate his birthday this weekend.

Consumer sentiment fell for the first time in four months, sitting about 5% below February at 63.4 but remaining 7% above a year ago.

This month’s decrease was already fully realized prior to the Silicon Valley Bank, at which time about 85% of our interviews for this preliminary release had been completed.

Sentiment declines were concentrated among lower-income, less-educated, and younger consumers, as well as consumers with the top tercile of stock holdings.

Overall, all components of the index worsened relatively evenly — primarily on the basis of persistently high prices, creating downward momentum for sentiment leading into the financial turmoil that began last week.

Jim Umpleby — Chairman & Chief Executive Officer

Well, thank you, Jerry. It's great to be back here at CONEXPO again after the last three years. But we introduced a new strategy for profitable growth back in 2017. It was based on a number of — of elements. The framework we used is what we call the Operating and Execution Model, which requires that our leaders look at our business at a much more granular level, understand by product, by market, by application where we're creating shareholder value and where we're not. And by providing that visibility, shining a light on each product, application, and market, we were able to challenge our leaders to improve the financial performance of those products that were underperforming in our view. And I think our team has done a very good job in improving the financial performance on a number of the products and businesses.

There were a few where we concluded that they were not either strategically or financially aligned with where we wanted to go, and so we made some divestments there. But even more importantly, that framework gives us the ability to bias our resources, investments in capital expense, and management attention in those areas that represent the best opportunities for future profitable growth. And I believe that Operating and Execution Model has played a large part in our improved financial performance over the last few years.

BLUE ROOM

+WEEKLY+

THURSDAY’S GLOBAL ZOOM

—

Thursday

March 16, 2023

12 PM

BLUE ROOM

GLOBAL MEETING #111

———————

Dear Blue Room,

We would love to see you all for Meeting #111 at 12 PM Mountain Daylight Time today!

Agend:.

Blue Room UpdatesII.

IcebreakerIcebreaker

Questions (Thanks to Nina!)

-- If you had to delete all but 3 apps from your smartphone, which ones would you keep?

-- A survey: Yes or No on daylight saving time?

F

U

N

D

O

N

E

IS LIVE

10% OF ALL BLUE ROOM REVENUES GO DIRECTLY TO FUND OUR NON PROFIT TOGETHERISM.

WE CAN ACCOMPLISH ANYTHING TOGETHER.

These materials do not purport to be all-inclusive or to contain all the information that a prospective investor may desire in considering an investment. These materials are intended merely for preliminary discussion only and may not be relied upon for making any investment decision. Any discussion or information contained in this presentation does not serve as a receipt of, or as a substitute for, personalized investment advice from Blueroom or your advisor.

This publication does not constitute an offer to sell or a solicitation to buy any securities in any fund, market sector, strategy or any other product. Investing is speculative and involves substantial risks (including, the risk of loss of the investor’s entire investment). Past performance is not indicative of future results, and there can be no assurance that the future performance of any specific investment, investment strategy, or product will be profitable.

For more information about us and our general disclosures contact us directly.